Accounting

A practice and body of knowledge concerned primarily with methods for: recording transactions, keeping financial records, performing internal audits, analyzing and reporting financial information to company management, and advising on taxation matters. It is a systematic process of identifying, recording, measuring, classifying, verifying, summarizing, interpreting and communicating financial information. It reveals profit or loss for a given period, and the value and nature of a firm’s assets, liabilities and owners’ equity.

Accounting provides information on: the resources available to a firm, the means employed to finance those resources, and the results achieved through their use.

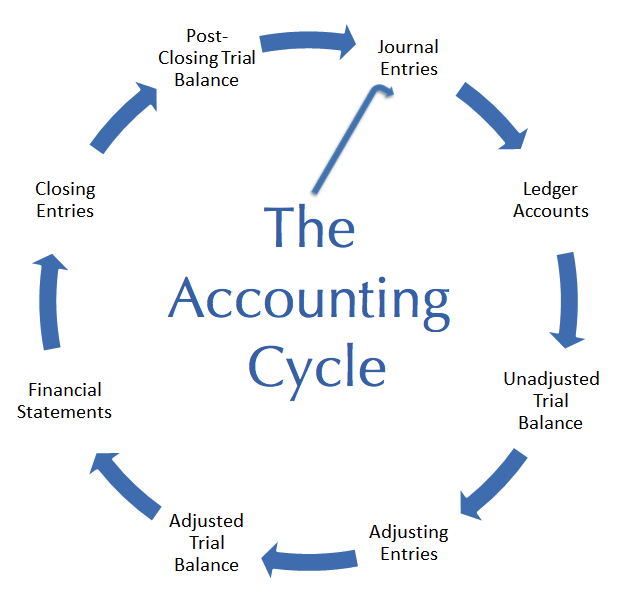

Accounting Cycle

A step-by-step process of recording, classifying, analyzing, and summarizing economic transactions of a business.

Accounting Equation

The accounting equation Assets = Liabilities + Equity is the foundation on which the entire double entry accounting system is based. The assets are the resources that a company has available for its use, such as cash, accounts receivable, fixed assets, and inventory. The liabilities are loans incurred for funding your business, and the equity is monies you have invested in your business or acquired from investors. The accounting equation reflects the balance sheet also know as the statement of financial position of a business at any given time.

Accounts Payable

An account that keeps track, by date, of vendors that you owe money to and how much you owe them.

Accounts Receivable

An account that keeps track, by date, of customers who owe you money and how much they owe you.

Accrual vs. Cash Basis

Under the accrual basis of accounting, transactions that affect a company’s financial statements are recorded in the period which the events occur, rather than in the periods in which the company receives or pays cash. Under the cash basis of accounting, revenue is recorded only when cash is received, and an expense is recorded only when cash is paid.

Adjusted Trial Balance

A list of the balances of ledger accounts which is created after the preparation of adjusting entries. It contains balances of revenues and expenses as well as assets, liabilities and equities.

Adjusting Entries

Journal entries made at the end of the accounting period to allocate revenue and expenses to the period in which they actually belong. This is done so that the books comply with the accrual basis of accounting.

Amortization

Method of reducing capital expenses for intangible assets by a fixed amount over a period of time for accounting and tax purposes. It is reflected as a book value in the reduction of an intangible asset on the balance sheet, and as an expense on the income statement. It is also very similar to depreciation – which is used for tangible assets, and to depletion – which is used with natural resources.

Assets

Anything of value that a business owns, including cash, accounts receivable, inventory and equipment. Assets are shown in the Balance Sheet.

Bad Debt

A debt that is not collectible and therefore worthless to the creditor. It is usually written off as an uncollectible expense after all attempts to recover it has proven futile.

Balance Sheet

A quantitative summary of a company’s financial condition at a specific point in time, including assets, liabilities and owner’s equity or net worth. It is divided into three (3) main parts: 1) Assets -the first part of a balance sheet showing all the productive assets a company owns, 2) Liabilities – the second part showing all the monies the company owes to creditors, lenders, etc., and 3) Equity – all the monies that the company owners have invested in the business plus/minus its income or loss.

Bank Reconciliation

The process by which a bank account balance as shown on the bank’s records is brought into agreement with the balance shown in your checkbook.

Bank accounts should be reconciled monthly.

Book Value

The value at which an asset is entered in company books and carried on a balance sheet. It is calculated by reducing the cost of an asset by the accumulated depreciation of the asset, amortization, or impairment costs made against the asset.

Bookkeeping

The process of recording financial transactions in their respective accounts. Bookkeeping can include invoicing, writing checks, bank and credit card reconciliations, payroll, filing of Federal, State and other taxes, and providing financial statements.

Break Even

The volume of business a company does at which the revenue equals the expenses. At this point a business does not have any profit or loss.

Cash Flow Statement

A summary of the actual or anticipated incomings and outgoings of cash in a firm over an accounting period – month, quarter, year. It answers two (2) questions: 1) Where the money came or will come from?, and 2) Where the money went or will go?

Cash flow statements assess the amount, timing, and predictability of cash-inflows and cash-outflows, and are used as the basis for budgeting and business-planning. The accounting data is usually presented in three (3) main sections: 1) Operating-activities (sales of goods or services), 2) Investing-activities (sale or purchase of an asset, for example, and 3) Financing-activities (borrowings, or sale of common stock, for example). These sections show the overall (net) change in the firm’s cash-flow for the period the statement is prepared.

Chart of Accounts

A list of accounts used when grouping accounting transactions. Account numbers may be used to identify each account, as well as organize financial reports in a specific order.

Client Preparation

A client usually needs the following for bookkeeping entries:

- Sales Invoices, paid and unpaid

- Bank Statements with returned checks, if available

- Check stubs

- Bills, paid and unpaid

- Receipts for expenses indicating what the expense is for. For example, rent, auto, etc.

- Credit card charges, indicating a description of the expense

- Expenses for meals including tips; marked name of person(s) involved, and date if not clear on the receipt.

Cost of Goods Sold

The direct costs associated with the production of goods for sale, or direct services for service-based businesses.

Credit Memo

Document issued by a seller to a buyer to reduce payment already made usually towards an Invoice. This amount is kept in the sellers books and applied against new Invoices for the respective customer.

Current Assets

Those assets that can be easily turned into cash, such as accounts receivable, and is expected to be converted to cash within a year.

Current Liabilities

Those liabilities or monies that you owe and expect to pay within a year.

Depreciation

The process of allocating to expense the cost of an asset over its useful life, in a rational and systematic manner.

Equity

The ownership interest in a business which is the difference between the value of the assets and the cost of the liabilities.

Escrow

A deed, bond, or other document kept in the custody of a third party, and takes effect only when a specified condition have been met. It is an independent neutral account by which the interests of all parties involved are protected.

Fair Market Value

The amount for which an asset could be bought or sold, in a transaction between a willing buyer and a willing seller. In other words, it is the selling price for an item to which the buyer and the seller can agree.

Financial Statements

Statements that describe the financial condition of a business. Such statements include the Income Statement, Balance Sheet and Cash Flows. These statements are usually prepared monthly, quarterly or annually.

Fixed Assets

Those assets that are purchased for long-term use and are not expected to be converted quickly into cash, such as land, buildings, and equipment.

GAAP

Generally Accepted Accounting Principles is the standard framework of guidelines for financial accounting used in any given jurisdiction. It is widely used in the United States, and dictates the recording and reporting of accounting information.

Gross Profit

The total income of a given period minus any direct cost (Cost of Goods Sold) associated with the income. It is the amount reported and shown on the income statement before administrative and other indirect company expenses are deducted. See IRS article “Figuring Gross Profit” for more information.

Income Statement

A financial statement that lists the revenues, cost of sales, various expenses and net income or loss. An Income Statement is also referred to as a profit and loss statement (P&L).

Liabilities

Liabilities are amounts that a business owes to its creditors, employees, or tax agencies. Liabilities are recorded on the balance sheet and can include accounts payable, loans, taxes, wages, accrued expenses, and deferred revenues. Liabilities are either current or long-term; current liabilities are debts payable within one year, while long-term liabilities are debts payable over a longer period.

Net Asset

Net asset is the sum of the total assets owned minus the sum of the total liabilities owed. In a sole proprietorship, the amount of net asset is reported as owner’s equity. In a corporation, the amount of net asset is reported as shareholder’s or stockholders’ equity.

Net Profit/Loss

The total income of a given period minus all expenses for that same period. It is usually the last item listed on the income or profit and loss statement, and will reflect a profit if the total income is more than the total expenses, and a loss if the total expenses are more than the total income.

Owner’s equity

The ownership claim on net assets is called owner’s equity in a sole proprietorship. It is equal to total assets minus total liabilities.

Revenue

The total amount of money received by the company for goods sold or services provided during a certain time period. It also includes all net sales from the exchange of assets, interest and any other increase in owner’s equity and is calculated before any expenses are subtracted.

Shareholder’s Equity

An ownership interest in a corporation in the form of common stock or preferred stock. It is calculated by taking the total assets minus total liabilities. Shareholder’s equity is also referred to as net worth.