Doing your own small business bookkeeping can be a very simple process; however, there are things that must be in place to ensure you are doing it correctly so you can retrieve accurate reporting from which to make good business decisions as well as file accurate taxes.And no, there is no way to avoid bookkeeping if you are running a legitimate business. You can hire a New York City bookkeeper to do your bookkeeping in-house or outsource your bookkeeping to a bookkeeping and accounting Firm – like ours, but your business bookkeeping must get done. Why? Because bookkeeping is an important part of running a business. It allows you to track the financial health of your business as well as keep your business in compliance with the relevant tax authorities by filing accurate and timely taxes.

Doing your own small business bookkeeping can be a very simple process; however, there are things that must be in place to ensure you are doing it correctly so you can retrieve accurate reporting from which to make good business decisions as well as file accurate taxes.And no, there is no way to avoid bookkeeping if you are running a legitimate business. You can hire a New York City bookkeeper to do your bookkeeping in-house or outsource your bookkeeping to a bookkeeping and accounting Firm – like ours, but your business bookkeeping must get done. Why? Because bookkeeping is an important part of running a business. It allows you to track the financial health of your business as well as keep your business in compliance with the relevant tax authorities by filing accurate and timely taxes.

What is Bookkeeping?

While accounting is the process of interpreting and communicating financial information, bookkeeping is the systematic process of identifying, classifying, recording, organizing, verifying, and managing daily financial transactions of a business.

How to Get Started With Your Own Bookkeeping

Having a defined framework is essential to starting and maintaining an effective bookkeeping system. In this article, we will be outlining 5 important steps that will help you as a small business owner, set up and maintain a proper bookkeeping system.

1. Choose an Appropriate Accounting Software

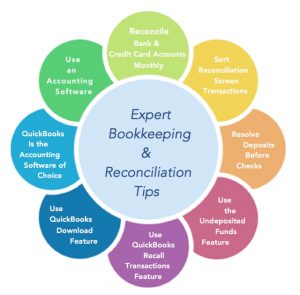

Accounting and bookkeeping software makes it easier to do bookkeeping. Some accounting software such as Sage 50 require extensive accounting and bookkeeping knowledge in order to use it correctly, while others such as QuickBooks allows you to use it with basic accounting and bookkeeping knowledge. It is very flexible, multi-functional – integrating with multiple apps, and allows for the production of a myriad of reports. Whatever you do, do not use an excel spreadsheet to do your bookkeeping, because not only is it inflexible, but it does not allow for the reconciliation of the accounts, and as such it has a large margin for error. Reconciliation is central to the bookkeeping and accounting process and a good bookkeeping and accounting software provides for the reconciliation of bank, credit card, loan accounts etc.

2. Set Up a Chart of Accounts

The Chart of Accounts is the backbone of the accounting and bookkeeping system. It is where information is stored to be retrieved via reports and thus need to be associated with the right account type in order to appear on the right reports and in the right places – making the reports correct. The Chart of Accounts should be specific to your business and workflow, however, every transaction must fall in one of five categories of accounts: 1) income, 2) expense, 3) asset, 4) liability, or 5) equity.

- Income account:This account records all the revenue the business generates for example revenue from the sale of inventory.

- Expense account: This account records the cash outflows from the business for example payments of salaries to employees.

- Asset account: This account records all the resources owned by the business for example property and inventory.

- Liability account: This account records all the debts and financial obligations the business owes for example a business line of credit.

- Equity account: This account provides a financial representation of the ownership balance of the business for example all business assets minus all business liabilities.

A good bookkeeping software will have a general Chart of Accounts to get you started and you can easily customize it to suit your unique business needs.

3. Separate Your Business & Personal Finances

Keeping your business and personal bank and credit card information separate will not only save you the headache of being extremely careful with each transaction every time you are entering them, but it will ensure you are getting accurate business reports from which you can make informed business decisions as well as using accurate information to file your taxes. Keeping your business financials separate from your personal finances will also help protect your assets in the case of any legal actions against your business. Accounting and bookkeeping software such as QuickBooks allows you to setup more than one business or company, so you can setup your business and your personal in two separate QuickBooks areas.

4. Reconcile Your Accounts & Balance Your Books

Without reconciliation your bookkeeping is incomplete and the accuracy of your books is unknown. Your transactions in your software should be tallied and compared with the transactions on your bank statements for example, and they should all match up. In addition, when you compute each months’ debits and credits, they should match up. This will mean that your books are balanced and the bookkeeping process is complete. You may choose to balance your books at the end of every day, week, month, quarter, or year.

Once you combine the different account types, it should meet the accounting equation: Assets = Liabilities + Equity, but don’t worry, as long as you enter the transactions in their right accounts and corresponding category types, software such as QuickBooks computes it all for you.

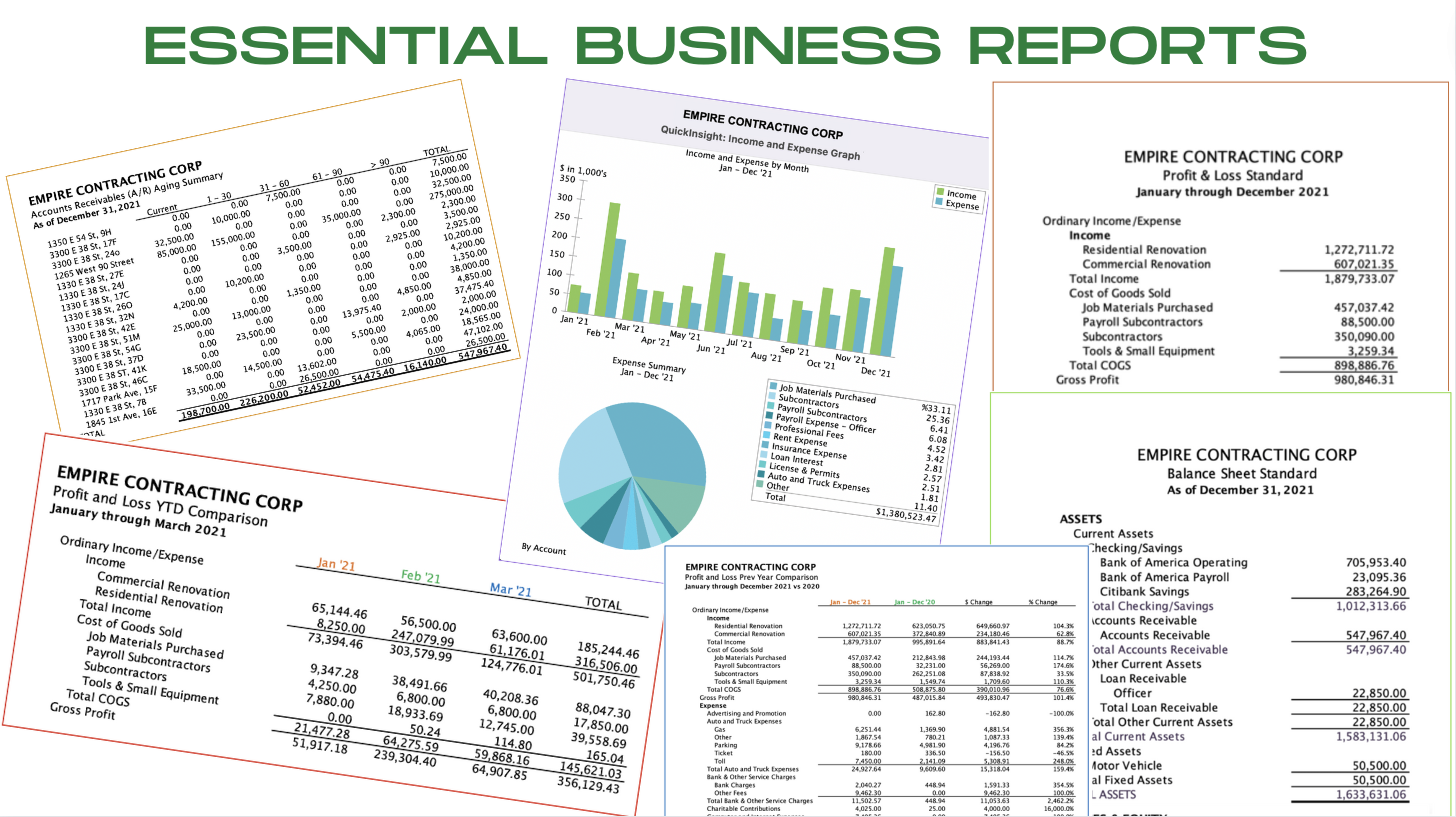

5. Generate Financial Reports Periodically & Analyze Them To See Where You Are Financially

It is very important to generate financial reports at regular intervals so you can get a clear picture of the financial health of your business. The three crucial financial reports are the balance sheet, profit and loss (P&L) or Income statement, and the cash flow statement.

The balance sheet summarizes the total assets, liabilities, and equity of the business. It indicates whether the business can expand or needs to reserve cash. The (P&L) statement or the income statement breaks down the revenues, expenses, and costs of a business over a period. It can enable you to compare sales and expenses and make accurate forecasts. The cash flow statement enables businesses to know their ability to fulfill short-term financial obligations.

Every business must get bookkeeping done regardless of how small they are, and the good news is there are qualified bookkeeping professionals available to handle the bookkeeping, if the business owner would prefer not to, or does not feel qualified enough to handle it.

At APO Bookkeeping, our bookkeeping services for small businesses protect business owners from making costly mistakes and provides valuable insights on how they can grow. You don’t have to be a math genius to start implementing bookkeeping for your business but you must be consistent and the foundation must be accurately laid. With this simple framework, you can start implementing bookkeeping today!

Hey Eugénie, thanks for sharing these very useful tips. I’m guilty of not doing #3 and 4 because I really didn’t know better. I co-mingled most of my funds which made it more difficult to get accurate reports, and I was also putting in all the transactions but not reconciling and thought all was well.

Wish I had this knowledge earlier, but I’m super grateful I found it now.

Let me go get on with correcting it now so I can move forward with an easier and more accurate flow.

All the very best!!!

You would be amazed to see how organized and accurate my bookkeeping system is now compared to where it’s been, and it’s all because of you. Your bookkeeping/QuickBooks training puts everything in perspective for me and even my CPA is loving the way everything is organized with accurate reporting now. He even asked for your contact saying he wants to send his disorganized clients to you so you can get them in order. LOL! There are so many people out here trying to teach before they learn but we all know you should learn before you teach. You obviously did that! You are well learned and an excellent teacher! Thank you 🙂