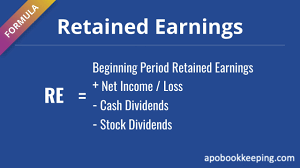

Retained Earnings, also known as “Accumulated Earnings” and “Unappropriated Profits” is one of the most important items on the balance sheet of a business financial statement. It represents the percentage of net income that is not paid out as dividends, but instead is kept “in-house” by the company.

Any item that impacts net income or net loss will impact retained earnings. Examples of items that would impact retained earnings include: sales revenue, cost of goods sold, depreciation, and general operating expenses.

How To Calculate Retained Earnings

Retained earnings is calculated by adding the net income from the current period to the retained earnings from the previous period and then subtracting any net dividends that were paid to shareholders.

It is calculated at the end of each accounting period and is based on the previous period’s figure. The resulting number can be positive or negative, depending on the company’s net income or net loss over time. A company with negative retained earnings has failed to earn a profit for a predetermined period, and is therefore retaining its losses. Failing to make a profit is not an uncommon occurrence for a business since failures will happen from time to time. However, if a company fails to earn a profit over several successive periods, the business owner should carefully evaluate the business, their earning potential, and the ambitions of the company.

What Retained Earnings Reveal About Your Business

Retained earnings can reveal much about a company. They are an important indicator of a company’s financial health and business performance. For example, a high and positive retained earnings might be a sign that the company has a strong business plan; however, a company with a history of low retained earnings may be able to access more financing.

How Retained Earnings Can Benefit Your Business

Knowing the amount of retained earnings can help a business owner understand the financial goals of the company. If a company has a high retained earnings, the owner can decide to take a larger percentage of investment income to support the company and reduce retained earnings balances.

Rather than distributing the profits to the owners, the retained earnings can be used to reinvest in the business or to pay off any debts the company may have.

The retained earnings account is important because it shows how much profit a company has made over time and how much of that profit has been reinvested back into the company.

For the best bookkeeping services in New York, APO Bookkeeping has you covered. We streamline your bookkeeping processes, ensuring that everything is kept updated, manageable, and above all – effective. Let’s have a chat—reach out to us today to learn more.

If you are a business offering goods and/or services on credit to your customers, or allow for partial payments/payment deposits, then you should create and issue your customers Invoices. This will allow you to track your customers balances for Individual Invoices in the accounts receivables ledger , as well as have a comprehensive view of your total outstanding customer balances. The Invoice connects the sales transactions to accounts receivables; the sales receipt on the other hand, does not.

If you require full payment at time of sale/service, then you should issue your customers Sales Receipts. Sales Receipts do not affect accounts receivables and thus will not allow for the tracking of any customer balances.

Businesses, such as restaurants and beauty salons that operate on a “buy/now pay/now” basis, do not need to Invoice their customers since they will not need to track payments owing to them – there won’t be any. Instead, they should issue sales receipts which is for the total amount of the sale.

Thanks to today’s technological advancement, these businesses have the option of using a Point of Sale system, and most can be linked to an accounting software such as Intuit’s QuickBooks, and have the transactions easily downloaded to QuickBooks instead of manually.

So there you have it! Use an Invoice when you need to track customer balances, and a Sales receipt when you do not.

If you are looking for reliable bookkeeping services in New York, we can help. APO Bookkeeping can provide one-time QuickBooks setup and training so that business owners can better understand their business finances. We can also do everything bookkeeping related for you. Check out our bookkeeping service packages and tell us what you think is best for your business.

Doing your own small business bookkeeping can be a very simple process; however, there are things that must be in place to ensure you are doing it correctly so you can retrieve accurate reporting from which to make good business decisions as well as file accurate taxes.And no, there is no way to avoid bookkeeping if you are running a legitimate business. You can hire a New York City bookkeeper to do your bookkeeping in-house or outsource your bookkeeping to a bookkeeping and accounting Firm – like ours, but your business bookkeeping must get done. Why? Because bookkeeping is an important part of running a business. It allows you to track the financial health of your business as well as keep your business in compliance with the relevant tax authorities by filing accurate and timely taxes.

What is Bookkeeping?

While accounting is the process of interpreting and communicating financial information, bookkeeping is the systematic process of identifying, classifying, recording, organizing, verifying, and managing daily financial transactions of a business.

How to Get Started With Your Own Bookkeeping

Having a defined framework is essential to starting and maintaining an effective bookkeeping system. In this article, we will be outlining 5 important steps that will help you as a small business owner, set up and maintain a proper bookkeeping system.

1. Choose an Appropriate Accounting Software

Accounting and bookkeeping software makes it easier to do bookkeeping. Some accounting software such as Sage 50 require extensive accounting and bookkeeping knowledge in order to use it correctly, while others such as QuickBooks allows you to use it with basic accounting and bookkeeping knowledge. It is very flexible, multi-functional – integrating with multiple apps, and allows for the production of a myriad of reports. Whatever you do, do not use an excel spreadsheet to do your bookkeeping, because not only is it inflexible, but it does not allow for the reconciliation of the accounts, and as such it has a large margin for error. Reconciliation is central to the bookkeeping and accounting process and a good bookkeeping and accounting software provides for the reconciliation of bank, credit card, loan accounts etc.

2. Set Up a Chart of Accounts

The Chart of Accounts is the backbone of the accounting and bookkeeping system. It is where information is stored to be retrieved via reports and thus need to be associated with the right account type in order to appear on the right reports and in the right places – making the reports correct. The Chart of Accounts should be specific to your business and workflow, however, every transaction must fall in one of five categories of accounts: 1) income, 2) expense, 3) asset, 4) liability, or 5) equity.

Income account:This account records all the revenue the business generates for example revenue from the sale of inventory.

Expense account: This account records the cash outflows from the business for example payments of salaries to employees.

Asset account: This account records all the resources owned by the business for example property and inventory.

Liability account: This account records all the debts and financial obligations the business owes for example a business line of credit.

Equity account: This account provides a financial representation of the ownership balance of the business for example all business assets minus all business liabilities.

A good bookkeeping software will have a general Chart of Accounts to get you started and you can easily customize it to suit your unique business needs.

3. Separate Your Business & Personal Finances

Keeping your business and personal bank and credit card information separate will not only save you the headache of being extremely careful with each transaction every time you are entering them, but it will ensure you are getting accurate business reports from which you can make informed business decisions as well as using accurate information to file your taxes. Keeping your business financials separate from your personal finances will also help protect your assets in the case of any legal actions against your business. Accounting and bookkeeping software such as QuickBooks allows you to setup more than one business or company, so you can setup your business and your personal in two separate QuickBooks areas.

4. Reconcile Your Accounts & Balance Your Books

Without reconciliation your bookkeeping is incomplete and the accuracy of your books is unknown. Your transactions in your software should be tallied and compared with the transactions on your bank statements for example, and they should all match up. In addition, when you compute each months’ debits and credits, they should match up. This will mean that your books are balanced and the bookkeeping process is complete. You may choose to balance your books at the end of every day, week, month, quarter, or year.

Once you combine the different account types, it should meet the accounting equation: Assets = Liabilities + Equity, but don’t worry, as long as you enter the transactions in their right accounts and corresponding category types, software such as QuickBooks computes it all for you.

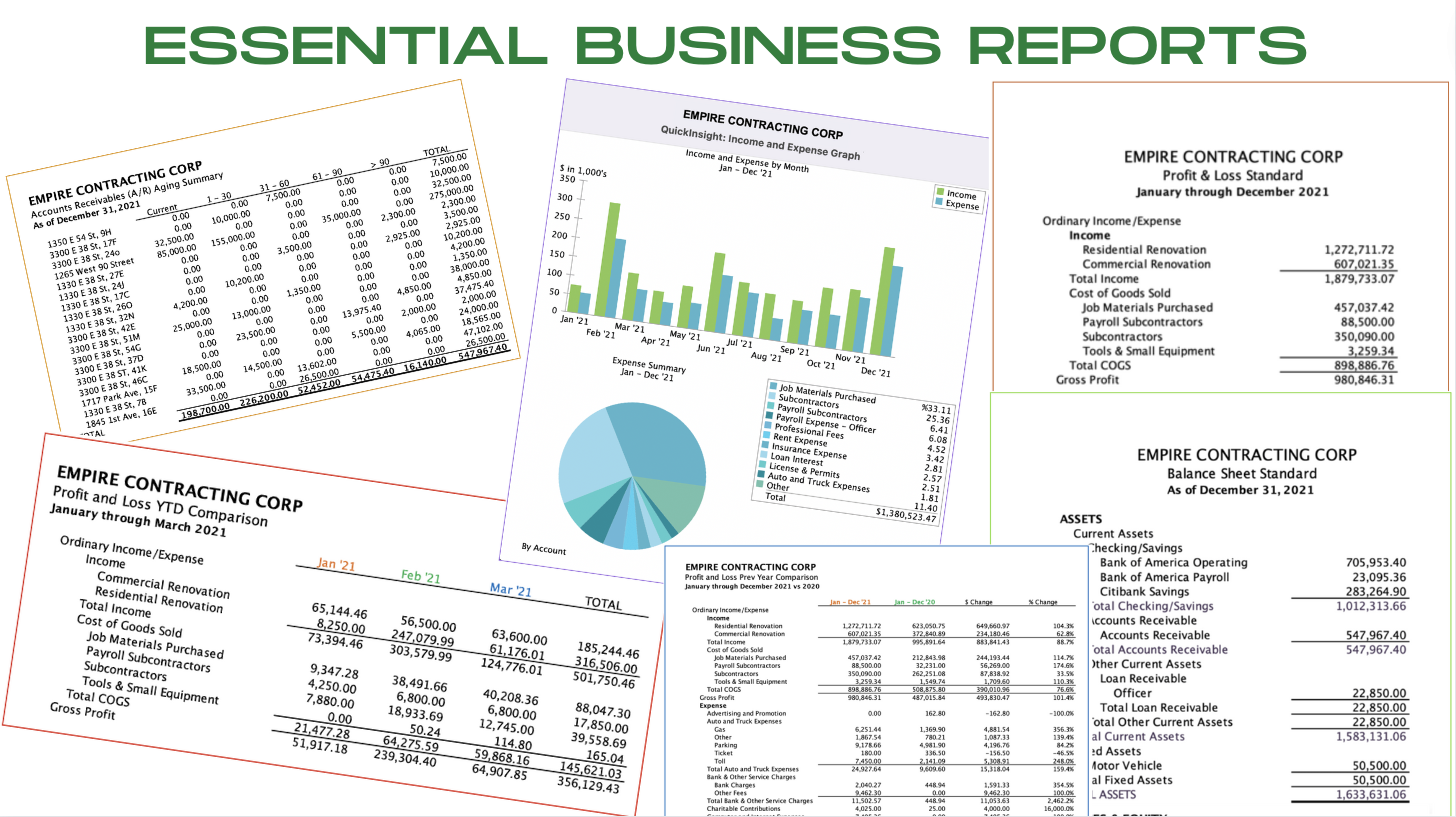

5. Generate Financial Reports Periodically & Analyze Them To See Where You Are Financially

It is very important to generate financial reports at regular intervals so you can get a clear picture of the financial health of your business. The three crucial financial reports are the balance sheet, profit and loss (P&L) or Income statement, and the cash flow statement.

The balance sheet summarizes the total assets, liabilities, and equity of the business. It indicates whether the business can expand or needs to reserve cash. The (P&L) statement or the income statement breaks down the revenues, expenses, and costs of a business over a period. It can enable you to compare sales and expenses and make accurate forecasts. The cash flow statement enables businesses to know their ability to fulfill short-term financial obligations.

Every business must get bookkeeping done regardless of how small they are, and the good news is there are qualified bookkeeping professionals available to handle the bookkeeping, if the business owner would prefer not to, or does not feel qualified enough to handle it.

At APO Bookkeeping, our bookkeeping services for small businesses protect business owners from making costly mistakes and provides valuable insights on how they can grow. You don’t have to be a math genius to start implementing bookkeeping for your business but you must be consistent and the foundation must be accurately laid. With this simple framework, you can start implementing bookkeeping today!

There is so much you can get from Excel spreadsheets, and no more! Don’t get me wrong, Microsoft’s Excel has its many purposes one of which is capturing information and making calculations including statistics with useful bars and graphs resulting in eye-catching, aesthetic presentations; however, it does not have the capacity to convert information from one report type to another, reconcile entries, or provide real-time bookkeeping and accounting stats, and therefore cannot provide the cross-reporting intelligence analysis that businesses need in order to facilitate strategic planning and make good business decisions. It is not enough to know how much profit has been made thus far for the current year, or how much your current expenses are; businesses must be able to look comprehensively at their business stance at any given moment, if being successful and staying in business for the long haul is their main goal.

Use an Integrated Financial Solution Software for All Your Business Accounting Needs

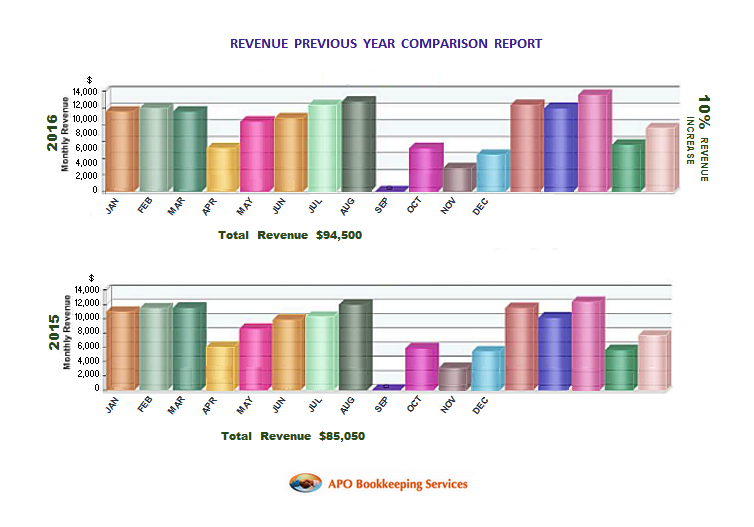

This is where cross-reporting, intuitive, integrated financial solutions software such as Intuit’s Software – QuickBooks, and Sage Peachtree come in. With an integrated financial solutions software, you enter the information once, and you get to use that same information in a variety of ways to pull insightful reports including, not only Cash Flow Analysis and Profit and Loss reports but also Previous Year Comparison Reports that can help you see where you have been, the strides you have taken, and how best you can improve your game plan moving forward. With Microsoft Excel, you will need to enter the information more than once – even if it means copying and pasting field items and re-configuring codes, it is very time consuming, non-productive, and limiting. According to Fran Burns – Contributor at CFO Tech Outlook, “It’s time to stop ignoring the ‘elephant in the room’ and focus on integrated solutions that enable one version of the truth.”

“The number one disadvantage of using Microsoft Excel for accounting is the lack of its ability to reconcile accounts, which is the most important aspect of accounting.” Eugénie M. Nugent

As a liaison working on the front line bridging the gap between many CPA’s, CFO’s and their clients, I have seen firsthand the dilemma they are faced with from clients who refuse to use anything other than Excel for their accounting, yet require accurate financial analysis and advice from their CPA’s and CFO’s based on the limited construct of Excel spreadsheets they have tabulated. As I have come to realize, many of these clients choose to stick with spreadsheets because they are intimidated by these software; even when they have delegated their bookkeeping, they feel a sense of not knowing what is going on behind the scene, and this unfamiliarity has kept many of them from stepping on board the integrated financial solutions software train. I have the responsibility to steer those clients to the right software, in order for them to be able to get what they need as far as their personal or business financial analysis – which their CPA will not be able to provide them with – if there financials aren’t compiled in a way such that relevant reports can be accessed and generated, and so I have developed one-on-one customized training modules for these business owners using QuickBooks, which has resulted in a paradigm shift.

Microsoft Excel is a multidimensional, multifaceted macro programming language software that has earned its place in the business world and the world in general; however, it is not an accounting software – was not designed with accounting in mind, and therefore should not be used as your main accounting tool. If you are a business owner who is serious about having the right information to help you make good business decisions, you must use an integrated financial solutions software for your accounting. If you must use Excel in your business reporting, use it to configure and house data that you have compiled using an integrated financial solution software.

Bookkeeping and Accounting can be boring! However, it is an essential part of your business as it gives you clear information about the status of your cash flow – how much money is truly available in your bank account for spending, who owes you money, who you owe money, how your business is performing overall and so it must be done. Many business owners who handle their own bookkeeping usually update their books on a monthly or quarterly basis; however, it is important to know where you are in your business at any given time – financially, and monthly or quarterly updating will not allow for such readily available information. Bookkeeping should be done in real time! Here are some of the benefits of real-time bookkeeping:

Real Time Bank Balances

In order to give you a true view of your available funds in your bank account, you must update your books on a daily basis. The balance your bank is showing as available at any given time, may not be as accurate as you think it is, unless of course you are using an accounting software such as QuickBooks Online and ensure daily updates. Without real-time Bookkeeping and Accounting your business cannot take into account outstanding checks that might affect your bank balance which the bank has not yet processed. Say for example your bank account balance shows a balance of $15,000 but you recently wrote a couple checks to your employees for your latest payroll, and your recurring rent payment through bill pay is not yet automatically initiated by your bank. Is your bank balance still $15,000? No, the true amount available in your bank is $15,000 minus any outstanding checks. Cloud accounting software such as QuickBooks Online or Xero will eliminate this shortfall as they both do an amazing job at tracking both the bank balance as well as your true available balance. However, this can only be effective if you use real-time bookkeeping and accounting procedure – daily updating.

Real-Time Cash Flow Analysis

It is very easy to overlook information that does not directly affect your business bank account such as business expenses afforded with personal funds. Employees reimbursement or business owner reimbursement may be omitted from your reports if they are not included in real time, which will undoubtedly give you inaccurate information and possibly a false sense of cash flow security when the cash isn’t really there.

“Without real-time bookkeeping and accounting you cannot gain a true perspective of your business stance, or your cash needs.” Eugénie M. Nugent

Real-Time Reporting

Bookkeeping and Accounting on a real-time basis offers you a greater level of information than if you updated your books sporadically. It allows you to have greater insight into your business performance by knowing you can generate a Financial Statement like a Profit & Loss in the middle of the month with real updated information. This is crucial to help you better understand if you are meeting your monthly monetary goals, as well as staying within your budget. Real-time bookkeeping update will help you predict how much cash is needed for ongoing expenses you might have by the end of a particular month, for example. Your accounts receivables and payables will be included in your reports – if you are operating on an accrual basis, making your reports more inclusive and true. Without real-time bookkeeping and accounting, you cannot gain a true perspective of your business stance or your cash needs.

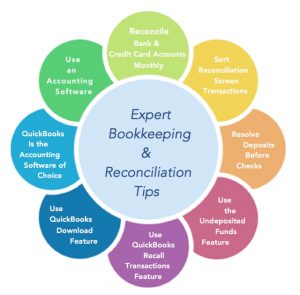

Reconciliation is a very important aspect of the bookkeeping and accounting process. It is also the only way to ensure your numbers are accurate. As such, reconciliation of the bank and credit card accounts should be done on a monthly basis, and a report of the reconciliation kept for your records. That said, reconciliation can be tedious especially if there are multiple accounts to reconcile and they are not done regularly. This where a software comes in handy! An accounting Software such as QuickBooks, will allow you to not only reconcile your accounts, but to easily download transactions from your bank and credit card institutions – into QuickBooks. Accounting software also allow you to have all your financial information grouped in one comprehensive system from which you can generate multiple useful financial reports. If you are using QuickBooks or thinking about using it, here are a few tips and tricks that will help you have a more pleasant, less onerous bookkeeping and reconciliation experience:

Take Advantage of QuickBooks Download Feature

QuickBooks download feature can go a long way in helping with your transactions input, as well as your reconciliations. After the initial banking and/or credit card online banking setup, you will only need to click one button called Update – periodically, in order to have your new transactions downloaded. You will need to review the transactions before adding them directly to the various QuickBooks register and accounts, but instead of manually entering all the information that pertains to each vendor or customer, you will only need to click one button for each transaction to be added to QuickBooks – in most cases. You may have to change the account that some transactions are associated with; however, that is minimal compared to entering every detail. This downloaded transactions process of easily adding information to QuickBooks, makes the reconciliation process easier. Manual entering can cause transactions to be missed or amounts incorrectly entered, but the download will enter them exactly as they should be, and so you will not spend time looking for a difference that could be due to $6,269 entered as $6,296 which is usually more difficult to locate. If you are using QuickBooks Online, you will have an added edge in matching the transactions because QuickBooks Online is Intuitive and will show you possible options for the transactions that would otherwise be elusive.

“The bookkeeping and the reconciliation process can be fairly simple if an effective accounting software is used, and proper procedures set up and followed.” Eugénie M. Nugent

Use the Undeposited Funds Feature

Reconciling the deposits on the statements with the deposits in QuickBooks can be an arduous task if Invoices were used and the payments received for those Invoices were not deposited to the bank in the amounts that they are in QuickBooks. In other words, if monies were deposited in the bank in one lump sum payment of multiple customers, and these payments were not grouped via undeposited funds and posted to QuickBooks bank register as such, it could be quite a task trying to figure out what deposits in QuickBooks make up a particular lump sum deposit on the bank statement. So, you want to make sure you are entering the transactions in QuickBooks with the reconciliation process in mind.

Resolve the Deposits Before the Checks and Other Payments

Like the deposits that are received from multiple customers and deposited to the bank in lump sum but not in QuickBooks, deposits from credit card merchants can also be problematic to reconcile. American Express, for example, groups weekend transactions together and deposit them as one lump sum deposit for the two days weekend sales, and so if you are manually recording some sales on a daily basis, that – topped with the payment portal payments can make it really difficult to match and reconcile. As you can see, reconciling these deposits could take some time, and you want to ensure sooner than later that all your deposits actually were deposited to your bank account. It rarely happens, but banks make mistakes too!

Use the Recall Transactions Feature Effectively

The recall transactions feature is a huge time-saver! After you have setup the preferences for QuickBooks to recall previous transactions information, QuickBooks will automatically recall the last transaction or account used for any vendor you have already paid. It can be a huge time-saving tool if used appropriately. For example, if you have an American Express Card, and you also accept payment through American Express Merchant Services, you can create three different variety of vendor names to make it easier to recall the transactions for each, rather than having to type in the different account information each time. Such as:

Vendor #1 could be called Amex-4566 (last 4 digits on your Amex Credit Card) – which you would use to handle payments from your checking account to your American Express credit card

Vendor #2 could be called Amex Finance Charge – which you would use to handle your finance charges assessed to your American Express Credit Card

Vendor #3 could be Amex Merchant Fees – to handle your merchant processing fees charged by American Express

By doing this, QuickBooks will automatically recall your Amex credit card payments as coming out of your checking account, Amex Finance Charges as being a bank charge expense, and Amex Merchant Fees as being a merchant processing expense. If you set up your QuickBooks this way, you will only have to make minimal changes – if any, to the recalled transactions.

“Get yourself a good accounting software, set up protocols as far as the procedures, and ensure you and anyone designated to your bookkeeping and reconciliation tasks, use them.” Eugénie M. Nugent

Reconcile The Smaller Accounts First

If you are new to reconciliation, or reconciling your accounts using a software, I recommend starting with the smaller accounts with less transactions so you can: a) get some practice, b) feel accomplished in reconciling it more quickly, and c) get a boost to take on the bigger challenge. For example, you may start with all the credit cards and loan accounts before moving on to the savings, payroll, and then the general checking account(s). Also, the larger accounts are usually impacted by the smaller accounts, and so you want to first focus on the accounts that have an impact on the general checking account(s). Another important thing to do, is to ensure transactions such as third-party payroll to companies like ADP and Paychex, are entered into QuickBooks before adding your downloaded transactions into QuickBooks. This will allow the payroll transactions to be matched up to your downloaded transactions in your download review window.

Sort The Reconciliation Screen Transactions

If you have a large volume of transactions, knowing how to find and clear them quickly is super important. QuickBooks allows for the easy sorting of transactions by amount – smallest to largest and vice versa, check number order, etc. Sorting by amount can be a huge time saver, especially when trying to match the deposits. If you have credit card merchant deposits coming into the checking account you probably have a lot of unique numbers. Sorting by amount by clicking on that column can make your QuickBooks reconciliation process much more effective while helping you work more efficiently. Also, sorting the checks and payments side of the reconciliation by check number will allow you to easily check the numbers in number order. In addition, when going through the transactions on the bank statement, it could save a lot of time if you check off the transactions by the different statement sections. There are a few banks that do not separate them, but if yours do, it could save a lot of time.

Bookkeeping and the reconciliation process can be fairly simple if an effective accounting software is used, and proper procedures set up and followed. However, it can be quite the opposite if none of this done. Get yourself a good accounting software, set up protocols as far as the procedures, and ensure you and anyone designated to your bookkeeping and reconciliation tasks, use them.

What accounting software are you using? And, what steps do you take to help simplify your reconciliation process?

The fact that you are reading this means you have thought about it. But would you have been interested in a “cloud based” accounting and bookkeeping application a few years ago? Probably not! Like myself and many small business owners, you were probably still trying to get your arms around the cloud and doubting that you would ever entrust your most critical financial data to some outside company. But times have changed. Online, or cloud financial applications are slowly but surely becoming the norm, and many small business owners are taking notice, particularly because of their benefits.

There are many cloud accounting and bookkeeping applications available on the market to date for small businesses. Some of them are: QuickBooks Online, Cheqbook, Xero, FreshBooks, Kashoo, Zoho Books and Wave. Most of these programs are pretty simple to use, and with only the bare basics of accounting, anyone should be able to use them. These programs also make it easier to have someone else do your bookkeeping while you maintain your Invoicing and receivables simultaneously from anywhere there is an internet connection. They can be accessed on a smartphone, tablet, or computer. This means that you have options! You can outsource your entire bookkeeping and accounting processes, or elect to have specific portions outsourced.

Benefits of Cloud Accounting

1. Cloud Based Accounting is Safe and Secure

When it comes to your company’s finances, nothing is more important than keeping your sensitive information from leaking out, which could have disastrous effects on you and your business. With a cloud based virtual accounting solution, your data is stored on a secure server. When you need to send data back and forth, it is done using only the highest available level of encryption, which keeps the data from being read – even in the unlikely event that someone could intercept the transmission.

2. Cloud Accounting is “Always On”

O the convenience of easy access! One of the reasons that cloud based accounting is becoming so popular is that it provides a level of coverage that you could only get otherwise by hiring an entire accounting department. Most small businesses cannot afford the expense of hiring even one full time staff member, and will generally bring someone in to do the books on a part time basis as needed. That may only be once per month to a few days a month, which leaves a lot of gaps if there are critical needs on the off days. With these applications you have the option of using a virtual bookkeeper and even accountant, which will undoubtedly cost less while keeping your accounts updated. Even at nights while you sleep, your accounts can be updated. You can choose to have a team assigned to you by some of these companies for full coverage, if you prefer to have the same company personnel rather than other remote bookkeepers do your bookkeeping. Regardless of how you choose to handle your bookkeeping, using any of these cloud accounting applications will allow you and whomever you give permission, to have access to your data 24/7 from anywhere with an internet connection.

3. Cloud Based Accounting Applications are Versatile

Cloud based accounting applications have something that only the cloud can provide. Because these applications are located online, they are better able to be integrated with many other applications that are designed to work with them, offering customized solutions to various business needs. Ecommerce and payment processing solutions such as Shopify, Paypal, Square etc. work seamlessly with these programs. QuickBooks Online has the widest market of these software applications, and as such, there are many more applications available that can be easily assimilated with it.

4. Cloud Based Accounting Allows for Seamless Collaboration

Since these applications are cloud based and hosted, they allow for easy and seamless collaboration. You and your business partner, for example, may be in different locations but need to look at and discuss your numbers. These online programs make this possible!

Downside to Cloud Accounting

1. These applications often become overloaded and thus slow running, depending on the time of day. During regular business hours of 9 through 5 when most businesses are open and staff working in QuickBooks, there may be times when it becomes really slow.

2. Cloud based accounting applications are sometimes inaccessible. There may be times when you have work to do but the application is inaccessible or unavailable for any number of reasons.

3. You Cannot Backup Your “In the Cloud” Data. Because these applications are not on your system, you cannot backup your data, and will need to wholeheartedly trust these companies to have your data available whenever you need to access it.

Technology has advanced in a myriad of ways, and people who are not excited about the new way of doing things are forced to either move with the time, or be left behind. Many accounting software companies who started out with desktop accounting software are moving rapidly towards closing them out altogether. Although you may have purchased the desktop edition and it is yours to keep, you may not be able to use it the same way you usually do. For example, if you use your QuickBooks desktop software to generate payroll and depend on the updates from Intuit to get them done accurately, you will not be getting those updates anymore. If you are only using it for financial record-keeping, invoicing, etc. then you should be ok with it. Otherwise, you will need to switch to the cloud. Eventually that is the only option we will have! So, it is probably a great idea to get on board and transition sooner than later.

My Personal Preference

Desktop hosted applications. Call me old-fashioned, but I like to feel that I have control over my financial data. But what good is having the desktop software when they are no longer supported by their makers who strip away the minimal functionalities they have, such as the ability to email your Invoices through the software for quick payments, and generate your employees payroll?

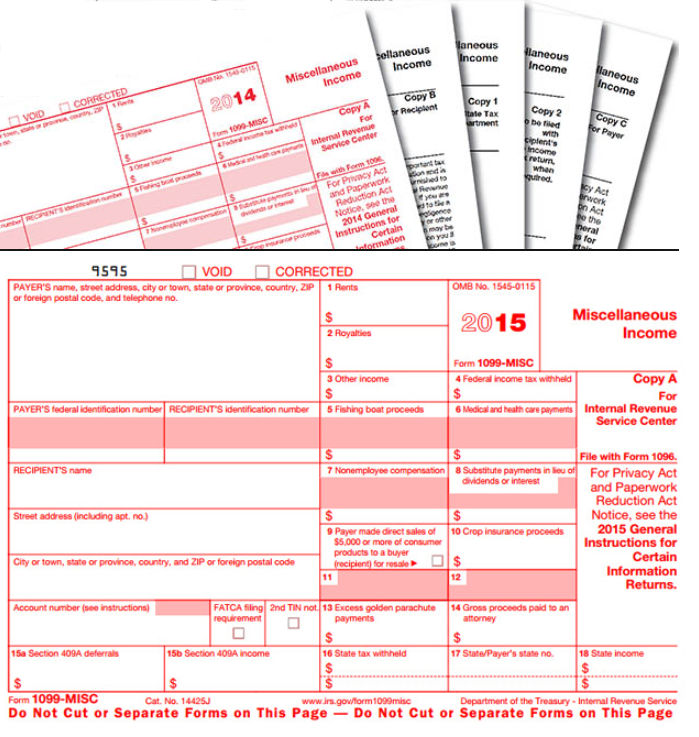

As with many tax forms 1099’s can be pretty confusing, especially now with more rules – and exceptions. There are multiple 1099 types as well as forms to accommodate them, but the most commonly used is the form 1099-Misc. As such, we will focus on the 1099-Misc. Here is a shortlist on the things that you need to know about 1099-Misc – and ensuring you are doing things right.

NOTE: The deadline for filing 1099 Misc Forms (Box 7 – Non-employee Compensation) has changed effective immediately, and the new deadline is January 31st following the reporting tax year. So, the deadline to file your 1099’s for 2020 tax year is January 31, 2021 – the same date you need to issue your 1099’s to your independent contractors by. If you do not have amounts in Box 7, then the deadline remains February 28th for paper filings or March 31st for electronic filings. (See 2020 1099 Misc Form instructions on IRS website)

WHO IS ELIGIBLE FOR A 1099

All subcontractors you have paid $600 or more to in a calendar year using any payment methods excluding credit card, debit card, gift card, or third-party payment network such as PayPal.

All service-based businesses that is NOT incorporated

An LLC or an LLP business may or may not be eligible. Follow the rule “when in doubt, send it out” to be on the safe side

Unincorporated Accountants and Lawyers are eligible; do not let them tell you otherwise

WHO IS EXCLUDED FROM RECEIVING A 1099

Corporations

Anyone you have paid with a credit card, debit card, gift card or a third party payment service like Paypal

Any company you have purchased a product from, such as office supplies, computers, etc.

The first step is requesting a completed and signed W9 form from your eligible vendors. The W9 form can be downloaded here and should be issued and collected BEFORE you make any payment to those vendors who are within the specified threshhold.

Use the information provided on the signed W9 form the vendors returned to you to complete your Form 1099’s. It should have: a) the name of the individual with the dba (if applicable) if a sole proprietorship, the name of the organization if a Limited Liability Company (LLC) b) the Social Security Number (SSN) or Employer Identification Number (EIN) of the sole proprietor, the Employer Identification Number if an LLC. c) an address so you can mail completed 1099’s out to them.

Print and mail out 1099’s to vendors by the deadline – usually January 31st of the following year for the previous year reporting, and IRS 1099 forms along with a form 1096 by this same deadline – January 31st. The 1096 is a summary transmittal form of the 1099’s, kinda like a cover letter to a resume. The forms can also be efiled to the IRS by a tax professional.

APO Bookkeeping uses QuickBooks to generate 1099 and 1096 forms for mailing, and also efiling forms if the number of 1099’s are above the threshhold for mailing which is 250 plus. If you will be generating the forms yourself, you can purchase preprinted forms at your local office supply store. You cannot print on regular printing sheets and mail as the forms need to be machine-readable for the IRS, and regular printing sheets are not.

There are multiple parts to the 1099-Misc forms. Below is the breakdown and where to send each:

Copy B and Copy 2 are for the independent contractor and must be provided no later than January 31st, following the year you are reporting

Copy A must be filed with the IRS no later than January 31st whether by mail or electronic filing.

Copy C is for you to retain in your files

WHAT ELSE DO I NEED TO KNOW ABOUT FORM 1099

If your 1099 forms contain a mistake, IRS can bounce it back to you. The most common mistake is the incorrect spelling of a name, or an incorrect tax identification number. Make sure forms are issued to the “exact” name that appear on the individual or LLC’s filing documents which hopefully is what they have sent to you on their form W9.

Also, try to pay vendors only one way! Do not send your website developer a check, followed by his or her next payment with a credit card, and then paying their next bill using Paypal. If you co-mingle payment methods, it will make calculating the amount you need to input on the 1099-Misc more difficult. Visit IRS website to view Other Types of 1099 Forms and their requirements.

WHEN ARE 1099 FORMS DUE

1099 Misc form for Non-employee Compensation (Box 7) is due to the independent contractor as well as the IRS by January 31st following the tax year – whether they are filed electronically or by mail.

All other 1099 Misc box categories and 1099 form types are due to the independent contractors by January 31st following the tax year, and must be filed with the IRS by a deadline of February 28th by mail or March 31st if filed electronically.

1099 forms must be postmarked no later than January 31st of the following year for the previous year reporting, or the next business day if the 31st falls on a Saturday, for all eligible vendors. They must be submitted along with a 1096 form to the IRS by January 31st if they are for Non-employee compensation – Box 7 on the 1099 Misc form, or by February 28th if for other boxes or other 1099 forms. The 1096 form is a summary sheet that lists the total amount of 1099’s you are submitting, and the total dollar amount of all of your 1099’s combined.

You can obtain a 30-day extension on the time to file 1099’s by filing IRS Form 8809, Extension of Time to File Information Returns. The form must be filed with the IRS by the 1099 due date which is January 31. The extension is not granted automatically. You must explain the reason you need it. The IRS will send you a letter of explanation approving or denying your request. As you can see, this extension request must be filed way in advance of the due date, as there is no way to know if the extension will be granted, and if it is denied you will be penalized for filing the 1099’s late.

As always, remember to stay in the know, in order to remain compliant in your business. 1099’s are just one aspect of the many requirements business owners must take care of, and we are here to help you understand these processes and activate you to pay attention to this (requirement) segment of your business which is also your responsibility.

If you have questions regarding 1099’s or need help getting them done, we are here to help you! Contact us today so we can get started! And if you’re looking for bookkeeping services in New York, reach out to us and let’s have a chat about it.

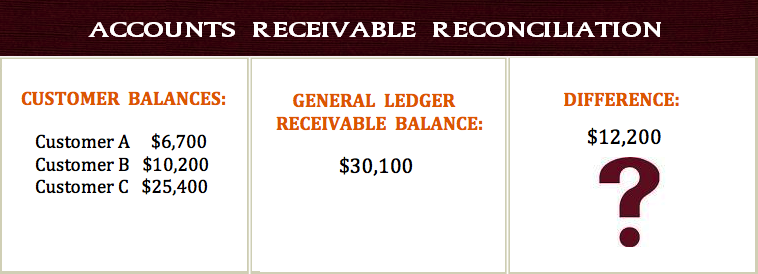

Managing your accounts receivable is very important because the timing of receivables plays a major role in your company’s cash flow. In addition, you want to ensure your customer balances are accurate, and your receivables current, based on the terms of service you offered your customers. Reconciling the individual customer account balances with the general ledger balance establishes the accuracy of the balance sheet asset. Reconciliation of your receivables should be done on a monthly basis – at least, as part of the month-end closing process.

What is Accounts Receivable?

Accounts receivable is the monies your customers owe you which is derived from the goods or services you have sold them or provided for them – respectively, on credit. When you sell goods or services to your customers on credit, the amounts they owe your business make up the accounts receivable balance in an accounting record called the general ledger. Their individual balances are found in the subsidiary sales ledger and listed in the aged accounts receivable report. This aged accounts receivable report will keep you apprised of the monies that are due, so you can reach out to those customers before they become way overdue. Reconciling accounts receivable means you are ensuring that the total of the individual amounts due from debtors equals the balance of the accounts receivable account in the general ledger.

How is Accounts Receivable Reconciliation Done?

You need to verify the general ledger accounts receivable balance, starting with the balance brought forward from the previous period. To do this: 1) Add the total of all invoices issued from the sales day book and deduct any credit memos issued. 2) Deduct the total payments received from customers – taking the figure from the cash book, and add any finance charges made. (If you post open credits (overpayments or advance payments from customers) to a separate general ledger account, the total at this point should be the same as the accounts receivable balance.) 3) Deduct open credits and add open credit refunds. 4) Check the final figure against the total of individual customer balances from the aged accounts receivable report. Any difference between the two balances must be investigated.

Common Reasons for Discrepancies in Accounts Receivable Reconciliation

The most common reason for discrepancies in accounts receivable reconciliation are journal or adjusting entries made directly in the general ledger and not reflected in the subsidiary sales ledger, or vice versa, and differing cutoff dates of the reports used. Two other possible reasons for discrepancies in the reconciliation numbers are; incorrectly offsetting customer and supplier contra-accounts, and posting to the wrong general ledger account.

When you have identified all the errors, you need to make the adjusting entries needed for the accounts to reconcile with the correct balances, and include a clear description of the reason for each transaction for auditing purposes. Where possible, reverse the incorrect entry and re-post it correctly, rather than posting the difference only, to make the transaction easier to follow. When all entries have been made, reconcile the balances again as a final check.

Incorrect accounts receivable balances will not only throw off your business financials as far as the receivables showing more monies owing than are actually owing, or vice versa, but can also make you lose valuable customers if you repeatedly send them statements with inaccurate balances. One time? May be not so much, but more than once could shout incompetent or dishonest.

Reconciling all your accounts on a monthly basis is the single most important thing you could do for yourself and your business. There are numerous software available to help make this process effortless, but regardless of the software or lack thereof, monthly reconciliations must be done in order to avoid costly mistakes.

Why reconciling your accounts is so important

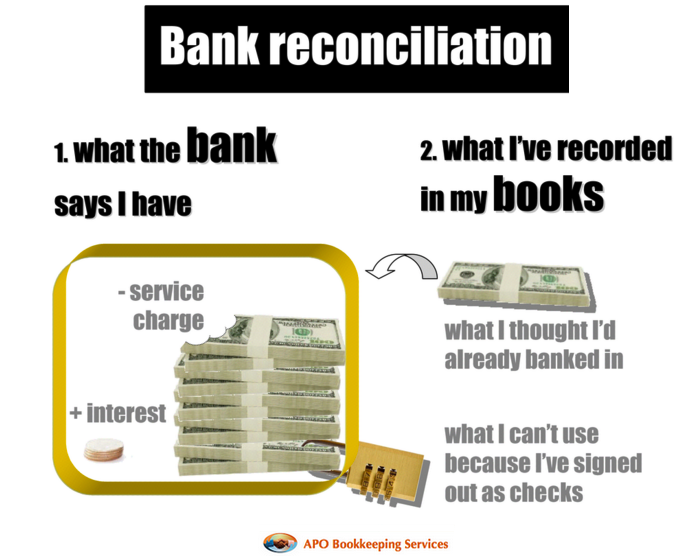

Reconciliation is so important because it is the only way to be certain your account balances are in agreement with your financial institutions, vendors, etc. Reconciling your accounts ensures that the actual monies spent matches the monies leaving an account at the end of a period, and that the actual monies put in also matches the monies coming into an account at the end of a period. When you reconcile your bank statement every month with your QuickBooks balance for example, you will become aware of checks that have not been cleared, and this will help you track down any potential missing payments. You will also become aware of any deposits you have made that are not showing up. This is rare, but it does happen! In addition, you can use your reconciliation statement to make sure your other company transactions are going through and have been calculated for the proper amounts.

There are aspects of your financials that reconciliation will not take care of such as personal monies you used up for the business, but have not recorded, as well as other assets and liabilities that may not have affected your reconciliations. So, reconciliations alone will not make your “books” accurate. You may need the help of a bookkeeper and CPA to get these aspects worked out; bookkeeper to ensure everything is recorded, and the CPA to analyze what is recorded and make the final call on whether the entries make the final books better or worse for the business.

It is imperative that controls – checks and balances, are in place to monitor the business banking and credit card transactions. For large firms you should have multiple hands assigned to cross-checking banking activities on a regular basis. For small businesses, you the owner should check your banking transactions – at least on a monthly basis to ensure everything is on par – even though you may have someone assigned to reconcile your accounts. When bank statements are not monitored and reconciled, the potential for undetected loss is high. Not all employees or accounting firms are honest, and you may not miss money that has been taken for some time. This is the reason some employees are able to embezzle hundreds if not thousands of dollars over time. Reconciling your bank statement helps you prevent losses and may indicate a potential problem in your accounting system.

What accounts can be reconciled and how to reconcile them

Any account that you get a statement for, showing a beginning and ending balance, can and should be reconciled. This includes: bank accounts, credit card accounts, loans and lines of credit accounts, and vendor accounts. There is also the internal reconciliation of many accounts, including customer receivables accounts.

Reconciling any account in software such as QuickBooks is a moderately easy feat. The time it takes to reconcile your accounts will depend on the accuracy of the transactions entered in your accounting system; if they were entered correctly – precise numbers and debit/credit accounted, your reconciliation should be done in a shorter time. If however they were not carefully entered, it may take you a longer period of time trying to locate the discrepancies. If this is the case, you may need to go transaction by transaction verifying your bank statement numbers with QuickBooks and marking each cleared as you go along. This can be tedious if there are many transactions; however, it must be done. You can see why it is vital to enter all transactions accurately to begin with. If you are using QuickBooks or other similar software, you should take advantage of the “download” feature. Initially, you will need to edit and select the right accounts as well as input the vendor or customer before you add or match each transaction; however, QuickBooks will begin to recognize each transactions that you have edited after a while and most importantly your numbers will be accurate with the correct corresponding debit or credit.

Using the ask my accountant account for questionable transactions

QuickBooks has a “Ask My Accountant” option in their chart of accounts that can be a huge ally in helping you reconcile. At times you may have transactions that you are not sure how to enter, or how to enter to be beneficial to your business. Any questionable transactions should be coded to “Ask My Accountant” so that you can continue with your reconciliations while having a conspicuous account to house them and have them easily accessed and rectified at a later date by your CPA.

So, reconcile your accounts on a monthly basis! You want to ensure that all the transactions are in your ledger and accurately accounted for. It is easy to forget to enter an expense or a payment when you are in a rush or if you have misplaced a receipt, so cross-checking against the account statement can be a good safety net for your own books. Doing so will ensure that you are getting paid—and paying people back—promptly, which in turn will help you keep other parts of your accounting in order such as your cash flow, profit and loss statement, etc. Of course you can trust your suppliers and creditors to charge appropriately, but everyone makes mistakes and are prone to err.

Doing your own small business bookkeeping can be a very simple process; however, there are things that must be in place to ensure you are doing it correctly so you can retrieve accurate reporting from which to make good business decisions as well as file accurate taxes.And no, there is no way to avoid bookkeeping if you are running a legitimate business. You can

Doing your own small business bookkeeping can be a very simple process; however, there are things that must be in place to ensure you are doing it correctly so you can retrieve accurate reporting from which to make good business decisions as well as file accurate taxes.And no, there is no way to avoid bookkeeping if you are running a legitimate business. You can