What Is Retained Earnings? How It Can Benefit Your Business

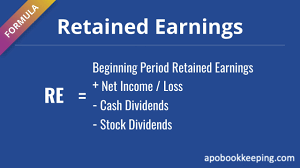

Retained Earnings, also known as “Accumulated Earnings” and “Unappropriated Profits” is one of the most important items on the balance sheet of a business financial statement. It represents the percentage of net income that is not paid out as dividends, but instead is kept “in-house” by the company. Any item that impacts net income or net loss will impact retained earnings. Examples of items that would impact retained earnings include: sales revenue, cost of goods sold, depreciation, and general operating expenses. How To Calculate Retained EarningsRetained earnings is calculated by adding the net income from the current period to the retained earnings from the previous period and then subtracting any net dividends that were paid to shareholders. It is calculated at the end of each accounting period and is based on the previous period’s figure. The resulting number can be positive or negative, depending on the company’s net income or net loss over time. A company with negative retained earnings has failed to earn a profit for a predetermined period, and is therefore retaining its losses. Failing to make a profit is not an uncommon occurrence for a business since failures will happen from time to time. However, if a company fails to earn a profit over several successive periods, the business owner should carefully evaluate the business, their earning potential, and the ambitions of the company. What Retained Earnings Reveal About Your BusinessRetained earnings can reveal much about a company. They are an important indicator of a company’s financial health and business performance. For example, a high and positive retained earnings might be a sign that the company has a strong business plan; however, a company with a history of low retained earnings may be able to access more financing. How Retained Earnings Can Benefit Your BusinessKnowing the amount of retained earnings can help a business owner understand the financial goals of the company. If a company has a high retained earnings, the owner can decide to take a larger percentage of investment income to support the company and reduce retained earnings balances. Rather than distributing the profits to the owners, the retained earnings can be used to reinvest in the business or to pay off any debts the company may have. The retained earnings account is important because it shows how much profit a company has made over time and how much of that profit has been reinvested back into the company. For the best bookkeeping services in New York, APO Bookkeeping has you covered. We streamline your bookkeeping processes, ensuring that everything is kept updated, manageable, and above all – effective. Let’s have a chat—reach out to us today to learn more. |