Many states are in a state of budget deficit and are looking for ways to fill that gap in the shortest time possible. They are searching really hard for new income source, and many of them may be on their way to finding one in the form of owed sales taxes to them – plus fees. They are creating means to get their monies in, such as the Nexus survey, and are on the prowl to collect on every dollar. That said, I have seen many small business owners who are disconnected from their bookkeeping/financial/taxes aspect of their businesses, which has left collected sales tax unnoticed and the filing requirements unmet. Some are also aware of their sales tax responsibility, but have taken it less seriously than other taxes such as payroll taxes. As with any tax requirements, there are fines associated with non-compliance, and you want to avoid those fines at all cost.

What is Nexus?

Nexus is a connection that a business has with a state, and it has to do with a form of presence. In the sales tax world, you owe sales tax to a state if you have nexus in that state and you are selling taxable items. The scary part for small businesses is what makes up nexus. See SBA’s contributor Caron Beesley “Sales Tax 101 for Small Business Owners and Online Retailers” for more sales tax/Nexus information. It is your responsibility to know if you are required to collect and file sales tax, and the correct way to go about it, such as filing for a sales tax permit prior to collecting sales tax.

It is advisable to keep a separate account for sales tax collected, and not include it with your income as it is not income but monies you collect on behalf of the relevant states, to subsequently turn over to them. If you have a bookkeeping and accounting software system setup for your business, this can make it very easy for you to setup an account so that that portion of monies received can be transported to that account, where it will be noticeable on the balance sheet as a payable and therefore owing by you.

Taxable in One State but Not in Another

Sales tax, like many other taxes, can be complicated and there are gray areas that are difficult to sort through. According to Caron, “As a general rule, if your business has a physical presence in a state – nexus, whether it’s a store, warehouse, office, employees or other criteria established by your state, then you must collect sales tax from customers in that state. If you do not have a physical presence in a state, then you are not required to collect sales taxes.”

Minimizing Sales Tax Audit Risk

You may receive a form that looks like a survey and asks innocent-looking questions such as: how many employees do you have? And, what state do they work in? The surveys do not look like they are from a state government but they may very well be. It is their way of getting you to admit nexus. Do not complete any of the surveys; it could expose you to a huge liability. It is always best to get a sales tax professional involved to help you determine the taxability of your items as well as to interpret nexus. Many states are hiring auditors and aggressively pursuing businesses, so due diligence in this area is prudent.

Get a grip on your sales tax and avoid getting blindsided

In an effort to combat holes in their budgets, many states are working to collect on monies owing to them, from all sources, by whatever means necessary. Sales tax is one such source of helping to fill that gap in budget, and so if you have collected sales tax on their behalf and have not paid it over, you need to do so at your earliest convenience to avoid hefty fines and fees. If you have not been collecting sales taxes, but should have been, get your paperwork in order and start doing so as quickly as possible.

If you need help getting a grip on your sales tax, there are many bookkeeping and accounting companies – like ourselves who are equipped with the knowledge and technical know-how to get your sales taxes under control. If you have not already done so, get a system setup where you can effectively track your collected sales tax, and pay attention to your sales tax filing. Reach out for the help you need, and avoid unnecessary penalties.

There are five (5) key questions that must be answered before making a decision to do your own bookkeeping versus hiring a professional:

How big is your business?

What is its growth forecast?

How complex are its finances?

What can your business afford?

Are you competent and knowledgeable enough in this field to handle your own bookkeeping?

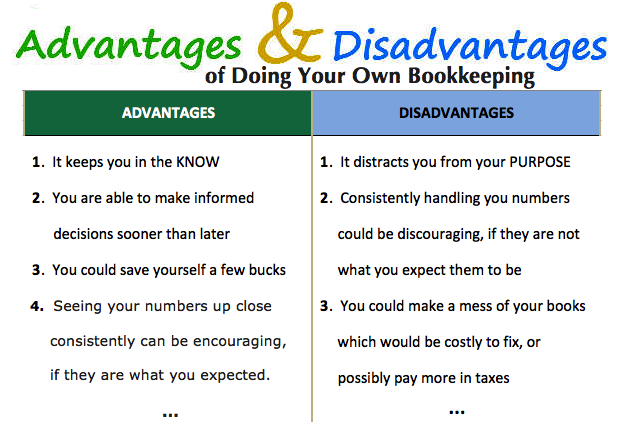

If you can answer the abovementioned questions honestly, your decision should be much easier to make. So, weigh the pros and cons of doing your own bookkeeping and make your decision.

If you are using a bookkeeping and accounting software such as QuickBooks, and you have a basic understanding of accounting principles as well as a CPA on board, you can indeed opt to get your own bookkeeping done. Also, bookkeeping can be time-consuming, but if you are equipped with the right accounting tools and knowledge, your bookkeeping time can be greatly reduced. Here are some advantages and disadvantages of doing your own bookkeeping:

Advantages

1) You are face to face with your numbers all the time, and as such you remain “in the know” and are able to make changes quickly – if necessary, to improve your business bottom line. Of course an efficient and knowledgeable bookkeeper will be able to give you reports explaining your business stance; however, it will not be the same as you intermingling with your numbers on a daily basis. You will make better business decisions because you always know where you stand financially. At any given time, you know who owes you money as well as what bills you need to pay. If a supplier or vendor has made an error you can act on it immediately instead of weeks or months when your bookkeeper brings it to your attention.

2) You are able to make informed decisions sooner than later. Doing your own bookkeeping gives you better control over your business dealings.

3) You could save yourself a few bucks.

4) Seeing your numbers up close consistently can be very encouraging if they are what you expected, or even better.

Disadvantages

1) Bookkeeping can be a real distraction to your business’ main purpose. You take time away from important business dealings that could be enhancing and improving your business bottom line. Bookkeeping is very time consuming and it happens to be one of those back-office tasks that can be done by someone else. Taking on the behind-the-scenes task of bookkeeping may not be the best use of your time. You can instead use this time to innovate, focus on making your product or service better, and grow your customer base. A huge part of a business success is maximizing its time.

2) If you do not have bookkeeping and accounting knowledge, you can make a mess of your books which can be costly – either to hire a professional to fix it, or you’ll pay too much in taxes. Bookkeeping and accounting can be learned; however, it is likely that you do not have the time to spend educating yourself on accounting basics o probably don’t want to. You would also need to master an accounting software which could turn into a very time consuming task.

3) Seeing your numbers up close consistently may be discouraging if they are not what you expected them to be.

Should You Do Your Own Bookkeeping?

Ultimately, the decision will be determined by how valuable your time is to you as well as your answers to the abovementioned questions. Be strategic in how you spend your time and money! Focus your time and energy on the areas of your business that you are truly passionate about. If bookkeeping and accounting is not a part of that passion, you can always delegate your bookkeeping. Maximize your time, and realize your business’ full potential!

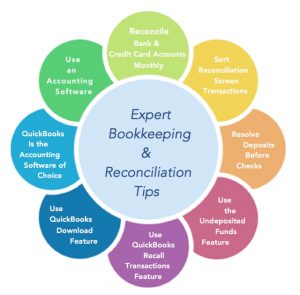

For any number of reasons, you may opt to do your bookkeeping on your own instead of hiring a bookkeeper in-house or outsourcing your bookkeeping. Like many things, there are advantages and disadvantages to doing your own bookkeeping, but with some basic accounting knowledge and a keen eye for detail you should be able to pull it off. Here are a few tips to help you as you do it on your own:

Use the Right Accounting System

Accounting is either cash-based, or accrual-based. With the cash method, you count the income when you receive it, and expenses when you pay them. Under the accrual method, you count income and expenses when they happen, and not when you actually receive or pay them – respectively. The other main difference between the two methods is the ability to budget accurately. Accrual method of accounting allows for better budgeting and planning because it looks at when liabilities are incurred and revenue earned and not when cash is paid. This method puts on the books liabilities that might otherwise be forgotten, like accrued interest. The cash method does not take accrued interest into account until it is required to be paid. This could put a strain on a small business that did not plan to pay out accrued interest balance, and is now faced with cutting expenses in other areas to have enough cash to pay the outstanding balance. The two methods have their advantages as well as disadvantages, and as far as filing taxes, the IRS only requirement is that you use the accrual-based system if your annual sales is more than $5 million or you store inventory.

Record transactions as soon as they occur

If you are using spreadsheets for your bookkeeping, or doing it manually on paper, you need to record your transactions as soon as they occur. If you are using an accounting software such as QuickBooks, you need to decide whether you will be recording transactions as they happen or adding them via the bank downloads later. Regardless of the method you use, keep your books updated at all times. Doing so will allow for little to no discrepancies, better workflow, and you will also have updated information on which to rely for decision making.

Record all business transactions

In order to have accurate numbers from which to make good business decisions, and file correct tax returns, you need to ensure all numbers affecting the business is accounted for and recorded. For example, if you are a business owner who sometimes uses personal funds for business expenses – and vice versa, you need to include those numbers in your bottom line.

Track Reimbursable Expenses

As a Small Business owner, it is very likely to sometimes use your personal funds to for pay business expenses. These monies should be reimbursed to you as well as recorded in the company’s expenses, and so there should be an account created to keep track of these reimbursables. Also, if your employees are construction workers or engineers who are usually in the fields and may use their funds to make small purchases that are immediately needed in order to continue their work, you need to collect those receipts and add them to the reimbursable account from which you will later repay them. Doing this is also important for accurate job costing.

Keep Accounts Categorization Simple

Overcategorization leads to miscategorization and ultimately inaccurate reporting. As a small business, you should be able to categorize your accounts in three to four sections:

1) Income – under which you can create subaccounts of your various streams of income

2) Cost of Goods Sold or Cost of Sales – under which you can create sub accounts for the employees salaries who are directly involved in the creation of the products you sell or the services you offer, as well as the products purchased to be used in the creation of your complete product for sale.

3) Operating Expenses – under which you can create a subaccount for Administrative Expenses and further subaccounts under Administrative expenses to list those individual accounts.

4) Other Expenses – under which you can create subaccounts to list other expenses that do not fall under any of the above categories.

The balance sheet accounts are usually fairly standard with three main sections: 1) Assets, 2) Liabilities, and 3) Equity each with their own subaccounts. You will need to create additional accounts on as needed basis. For example, if you loan money to your company, you will need to create a liability account to record these amounts the company owes you. Likewise if you borrow money from your company, you will need to create an asset account to reflect this.

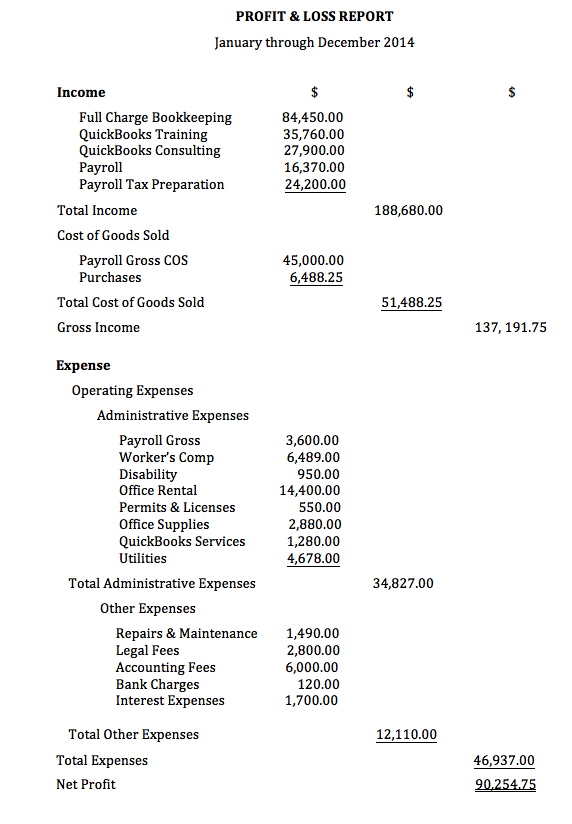

Here is an example of a Simple Profit & Loss Report or Income Statement:

Deduct Sales Tax from Total Sales

If you are a retail business that collect sales tax on behalf of the government, you should deduct these sales taxes from your sales. If you are using a software such as QuickBooks for your bookkeeping, and you do not track inventory in QuickBooks, you can setup this account as an Income account and set it as a discount so that it will be listed at the top of your Profit and Loss report and lessen from the total sales. Also, avoid penalties and interests and pay over your sales taxes as soon as they are due.

Keep Proper Records of Loans Received

Many small business owners need financial backing at their startup, and may take out a loan or two. These loans must be recorded and tracked in separate accounts, paying special attention to separating the principal repayment and the interest payment. The interest is an expense to your company and should be recorded in the expense section of your income statement or profit and loss report, while the principal is made towards your loan balance which will be in your liability section of your balance sheet.

Use Checks or Credit/Debit Cards Instead of Cash

Cash makes it harder to keep track of spending. Misplaced receipts, forgetting to document purchases all can be avoided if checks or debit/credit card payments are made. Not only will you have the amounts available to record, but you will also have details on uses of funds.

Reconcile all Business Bank & Credit Card accounts every month

This is one of the best business practices to employ! Reconciliation is a fundamental aspect of bookkeeping. Not only will you be able to catch any mishaps that occur; it will spread your workload and keep your books up-to-date-and accurate. Also, any mistakes on the bank’s or credit card company’s part that are not caught within six months, will not be able to be resolved. If you look on your statements, you will see that the banks include a reconciliation sheet and recommends that you reconcile your numbers with theirs. Reconciliation is the only way to ensure your numbers are accurate and your bookkeeping on par.

Let Payroll Specialists Handle Your Payroll

Payroll and payroll taxes can be complicated/intricate and not only do you need to ensure your employees paychecks are precise, but you must make correct payroll deposits as well as file accurate taxes. Payroll specialists are trained especially for this, and so they know the ins and outs, and are fully equipped to get this done accurately.

Keep a Proper Filing System in place

Not only is this good business practice, but you do not want to drive yourself crazy trying to find one document that is urgently needed – pronto. As a “do-it-yourselfer” it will greatly benefit you to keep a proper filing system where you will file all documents and paperwork in a manner that makes them easily retrievable.

Keep an Eye on Your Cash Flow

Cash is King for any business, and the lack of it is the reason so many small businesses fail. Know how much it takes to keep your business running on a monthly basis! Devise an accurate system of expenses and monthly obligations, and weigh them against your reliable monthly inflow of cash. Include an extra 20% of total expenses to your expenses for a bit of “cushion”. A budget and forecast report is a huge plus to create, maintain, and use as a financial guide.

Give Your Customers Options to Pay You

Providing your customers with a variety of payment options will not only make your customers happy as far as convenience, but it will allow you to get paid more quickly. In today’s fast paced world, convenience goes a long way! Some customers may procrastinate writing that check AND mailing it, or setting up that online bill pay. Allowing them the option to pay you via your submitted invoices will be a huge plus in helping your cash flow.

Invoice Customers on Time

The sooner you bill your customers the sooner you will get paid, and that will also help keep your cash flow up and your budget on track.

Pay Bills on Time

Pay attention to those vendors who are sacking a late payment fee to late payers. Take advantage of those terms of payments you get, but make every effort to meet them. The delay will help with your cash flow, but may accrue interest if not paid on time.

Have your vendors submit a completed and signed W9 form

For vendors to whom you have paid a minimum of $600 and above during the year who are not a corporation, you will need to report their payments to the IRS on from 1099-Misc at the end of the year. You will need specific information from them to include on this form such as their mailing address and tax identification number. It is best to keep W9 forms on hand, so that you can have your vendors complete them at the time you realize that the monies you are paying them are at this threshold. You should check your vendor balances to see if the monies you have paid them are amounting to $600 and above, as you may often write a check for under six hundred but may make more payments to them amounting to $600 and above throughout the entire year. Waiting for year-end to collect this information may be a daunting task, which many times – from my experience, has proven futile. You cannot file form 1099 without the vendors tax identification numbers, and of course you will need to mail their copies to them. If you pay your vendors through a Payment Portal such as Paypal or with your credit card, you will not be required to file or include those amounts on your 1099 as these companies are already reporting them on their 1099k.

If you have a system that allows you to quickly and easily retrace your company’s financial activities, your record keeping is effective. This includes keeping your invoices and checks in numeric order, not skipping check or invoice numbers, and keeping bank and credit card accounts separate. You should be able to retrace a year or years and have a clear trail of your company’s financial activities.

The best way to work as a “do it yourselfer” and not be overwhelmed, is to always keep every area of the business up-to-date. Designate a time to get the tasks that can be done later such as recording reimbursables and paying bills, and do the ones that cannot wait – such as Invoicing and attending to your customers first. Create a monthly chart with a daily workflow that you will be able to model everyday, and stick with it.

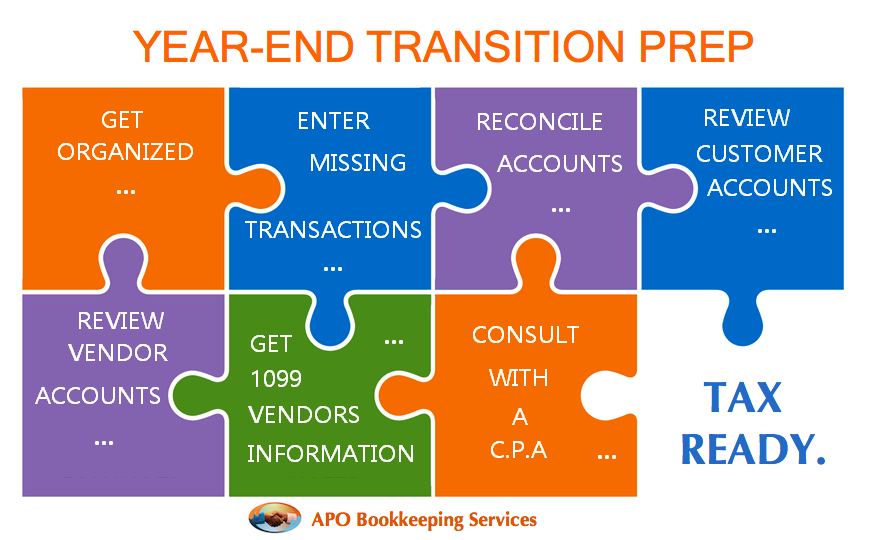

It is fast approaching year-end, and now is the time to take stock of your financials as far as your bookkeeping, especially if you are a one-man show. Yes, there are three (3) months to go before we actually hit the end of the year, but wasn’t it just year-end and tax time? Not quite sure where time is going, but the next three months will pass just like a breeze, and tax time will be here again not long after. Here are a few things you can start doing right now:

Create a filing system, if you don’t already have one, then organize and file your receipts, bank and credit card statements, and other paperwork. This will make it easier to retrieve information needed from them at any time, and also to stay complaint with tax rules. All year long, you receive paperwork and some of it will be needed to prepare your tax return. If you have not been, and do not file them away in an organized fashion, you will have difficulty locating them when they are really needed. The key is to choose a filing system in which you can easily file and subsequently retrieve documentation when needed, and use it. The biggest hassle at tax time is getting all the documentation together. Maintaining your documents in an organized fashion will not only help you avoid missing valuable deductions to which you may be entitled, but will also help ensure that your income tax return is complete and accurate.

Enter all transactions that have taken place since the beginning of the year in your accounting software, or on your excel sheet, if you are a spreadsheet user. I do not recommend spreadsheets be used as your main bookkeeping tool, as it is very limiting, and allows for more mistakes to occur. However, if your CPA or tax preparer has been and continue to accept your spreadsheets without complaints, then you should probably continue to use them. On the other hand, if your CPA or tax preparer has been ignoring you and not preparing your taxes on time after you have submitted your spreadsheet info, you can opt to use one of the many accounting software available on the market for desktop as well as online or “in the cloud”. Some of them will tell you to have a bookkeeper crunch your numbers, but others will push yours aside, and work on their clients with accounting-software-prepared reports first. Accounting software are more versatile, and you are able to generate all the relevant reports that a CPA or tax preparer requires. Also, reconciliation is one of the most important steps in keeping accurate books, and while it is possible with spreadsheets, it is more convenient and less error prone when done using accounting software.

Reconcile your bank and credit card accounts from the start of the year to date, so you will not be backed up and out of synch at year end. It is always advisable to reconcile your accounts on a monthly basis, not only to stay updated, but especially to ensure there are no mistakes on either side, and if there are, to catch and resolve them immediately. Reconciliation ensures that the bank and credit card numbers are in synch with your numbers; as such, you must keep a record of all your transactions, and reconcile them against your bank and credit card statements. Humans are prone to err and so are credit card companies and banks.

Review your customer accounts to ensure their balances are accurate, and also to locate possible bad debts. If you have a customer or customers that you believe are not likely to make good on past due amounts, now is the time to write off those bad debts as a loss on your books – accrual based accounting only. (For cash basis accounting, you can simply void the invoices deemed non-payable, as they are not included in your income.) Writing off bad debts may not be a total loss as you will be able to take a deduction for them providing you can show that:

The debt is bona fide – you have a contract between you and the customer that shows you provided goods and/or services to the customer, and expected to be paid or repaid. If you do not have a written contract but have an Invoice along with correspondence to show that you have been communicating about the debt and there was a promise to pay, then that should suffice as proof that the debt is legitimate.

You have a basis in the debt – you already included the amounts owing in your business’s gross income. You have to treat the money owed as paid, in order to make a claim for bad debt deduction. This happens when you do the write off and transfer the debt from owing to paid – from accounts receivable to bad debt expense.

The debt is business related – your Invoice and written communication should be enough to prove the debt is business related.

The debt became entirely or partially worthless – you have to show that you took all reasonable steps to collect the debt. Reasonable steps could be multiple emails and/or phone calls on various dates, you do not have to sue the customer in court.

Review your vendor accounts to ensure the balances are accurate, and to get caught up on any monies you owe that may be incurring interest. It is always good to stay on top of vendor accounts, at least on a monthly basis, especially those that attract interest for late payment. However, if you review and make overdue payments now, you may be able to save a few dollars in late payment interest. Also, if you have purchase orders for which you have received items but not yet billed for, now is a good time to get the numbers in for those inventory.

Make contact with vendors who are eligible for 1099 and ensure you have their pertinent information from which to generate their 1099’s as well as correct addresses to mail them. If you paid anyone for services amounting to $600 and above during the year, you are required to issue them a Form 1099 by January 31st of the following year, and you cannot file them without each contractors social security or federal ID number and accurate addresses. Form W9 should be given to new subcontractors and independent contractors to complete and sign upon hiring, but if you have not done so, now is the time. You do not want to have the hassle of tracking down subcontractors at year-end when the information is urgently needed, and you are extremely busy.

If your business has undergone any changes and you are not sure how it will affect your taxes, schedule a consultation with a CPA. You will obtain advice relevant to your business as well as information that can save you time and money at tax time.

Whether you are an individual with a W-2 job, a self-employed small business owner who earns 1099 income, or an established business with employees, now is a good time to review your current tax and financial situation – and look ahead at the rest of the year and into upcoming tax season. If you stay on top of your bookkeeping, you will have a hassle free tax period.

The above-mentioned are just a few things that you can do to help set the tone for a hassle free tax period, and are by no means exhaustive. You can assess your business based on its type, and needs, and start taking stock now instead of later.

A shredder is one of the most essential items for any business or individual to have and use, yet one that is highly overlooked. Confidential information are almost always included in our correspondence, and some of them are not always necessary to keep. These unwanted paperwork are often tossed into the trash without any thought about how they will be handled or where they may end up. With identity theft on the rise, extra precautionary measures must be taken to minimize the risk of you being the next victim. Anything that can identify you, or any financial account papers that you have, must be shredded beyond recognition. Today’s identity theft criminals are highly sophisticated, and getting your information in their hands could change your financial landscape and possibly take you months and sometimes years to recoup.

Important Shredder Features:

Cross-cut capability – some shredder simply take sheets of paper and cut them into dozens of long, narrow vertical strips the length of the page and although it is difficult to reassemble these strips, it is not impossible! Purchase a shredder with cross-cut capability, which cuts these strips horizontally as well as vertically, or a cross-cut shredders that cut paper into micro diamond-shaped pieces which are even more challenging to reassemble. Shredders with intricate cutting patterns are way more secure.

Multiple pages simultaneous shred – shredders are rated by how many pages they can shred at a time. For example, a single-page shredder requires you to insert only one page at a time. A ten-page shredder will shred a stack of ten pages at a time, and so on. A higher page rating means less work for you, as well as a lower risk of running the unit at its maximum capacity which can cause overheating over time with excessive use. Think about it! A unit rated for ten pages requires ten insertions to get rid of a stack of 100 pages, while a single-page unit requires 100 insertions!

Ability to Shred Credit Cards, Compact Discs, and Staples – simply cutting up old credit and debit cards into small pieces and tossing them in the garbage is not a proactive way to safely discard of your cards. It’s very easy for ID thieves to reassemble and use them, especially if the card being disposed of is a replacement card with the same account number as an existing card. Most modern shredders can shred credit cards with the same cutting efficiency that they shred paper, with the only exception that they must be singularly inserted. Some shredders can also shred CD’s and DVD’s that may house sensitive financial or personal information.

The point here, is to purchase and use a shredder to get rid of your documents you no longer need that contain highly sensitive information. Why take unnecessary risk when there is a simple solution?

In the same way most of us get out of bed each day and look forward to carrying on our productive lifestyle, there are some who get up with the same enthusiasm to set in motion their disastrous, destructive plans of varying degree such as hacking. You may have already been directly affected by the password thefts at LinkedIn last year or Evernote this year, or have had your own social media account, email, website, network, or computer hacked. What’s worse is that many of you have been hacked but don’t even know it.

So how can you minimize the damage and risk of hackers? Below are several tips – some familiar and some not so much. As you go through the list, check off the ones you’re already doing and make a list of new ideas to implement to protect your business and personal assets.

Don’t Sign Your Life Away

Your signature might look great in a graphic in your email signature line, your website, or your newsletter, but it’s a huge risk. You’re giving away your handwriting, and forgers can easily replicate, master your handwriting, and impersonate you. To reduce identity theft, don’t publish your real signature anywhere.

Help Secure Your Money

Implement strong passwords on all of your financial accounts: banks, credit unions, PayPal, credit cards, and your accounting system. Of course it’s painstaking to keep up with the various passwords we use on a regular basis, but do not use the same password for your financial accounts anywhere else, especially on social media! If possible, use a different password for each account to further reduce the risk of all of them being hacked.

Put Some Thought Into Your Passwords

Do not use your name, your pet’s name or your kid(s) names in your passwords. There’s just too much information available publicly to do that safely anymore.

Use a mixture of letters, numbers, capital letters, and special characters – if they are allowed.

Make passwords long! The longer the password, the more secure they will be.

Change passwords at regular intervals – on a quarterly basis minimum, to be on the safe side.

Password Storage

Most apps that help you save time with passwords are NOT safe! Here’s what I do and don’t recommend:

DO:

Password-protect your computer, even though you don’t have to.

Keep a separate file of your passwords on your computer, but DO password-protect that file and make sure it is not shared with anyone on a network. Also, name the file something totally unrelated like fishing trip, my letters, or favorite recipes; do not name it “passwords.doc!” You can also opt to keep a record of your passwords offline, but be sure to lock it up in a safe.

When you make file and disk backups, be sure those are locked away and password-protected too. They will no longer have your computer’s password to protect them.

DON’T:

Don’t give in to your browser or any website when they ask to remember your user ID and password, especially for your financial accounts or client information. All of the major browsers have been hacked – Internet Explorer, Chrome, Firefox, Opera, and even Safari.

If you use password management applications, proceed with caution. Be sure you have properly vetted their security claims. Most of them are simply form fillers that are not safe.

Maintain Active Subscription to An Internet Security Suite

These software are designed to not only get rid of malware, spyware and other hacking devices, but also to detect upon attempted intrusion and block them all. Software such as Norton Internet Security

are the best at keeping your computer and personal information safe. I have used it for years and continue to do so because of its tight security measures and reliability to protect my privacy.

Monitor Vulnerable Applications

Avoid leaving vulnerable computer ports open and unattended, including: chat, messaging, FTP (file transfer protocol), Skype, webinars, Google hangouts, video sharing, and such like. It’s like having all the doors and windows of your home unlocked; an intruder has a lot of choices for easy entry. When you are on these more vulnerable connections, shut the others down and close the applications you don’t need. You should also ensure you logout when you are done using the program or will step away for a while.

Install Your Software Updates

As soon as a hacker has found a new exploit, the software companies will learn about it and make an update available within days. The hacker community is tight; other hackers will look for software that is not updated and exploit the hack. Avoid the copycat hackers by staying on top of your software updates; not just your anti-virus, but also your Microsoft and other similar software updates. Doing this, will eliminate a great deal of the risk out there.

Separate User Accounts

If multiple team members need to access your software, consider setting up additional users rather than having one account. If one person gets hacked, the others will likely still have access and can react quicker to the intrusion.

Take Advantage of Two-Step Verification

Opt to use two (2) step verification system, even if it is not mandatory. You know those annoying security questions that you have to setup and must answer in order to gain access to some bank accounts online? Those are mandatory, thank goodness! But there are many other instances where it is not a requirement but optional; opt to use them as they are only meant to further secure you and your personals.

When you sit down at your computer or fire up your latest device, security is probably the last thing on your mind. You want to check your email, catch up with friends on social networks, play some games, purchase online goodies, or just attend to your business. The problem is, you actually need security! That new game, may be infected with malware, and the hilarious post from your best bud may actually have been planted by a hacker. If your computer and devices are not protected, neither are you; a data-scraping bot could well use your online shopping trip to steal your credit card info. and create havoc in your life.

Make the necessary changes, and stay safe out there!

Depending on the type of business you are operating, you may not have a vast amount of bookkeeping to be done on the first day – or even week you open for business; however, you should setup a bookkeeping and accounting system at your earliest, and make an effort to document all transactions starting on the very first day. This may not be an easy feat since you are just starting up, but in order to not get lost in your financial tracking and status, and also be in the right with the relevant tax authorities, you need to get an early grip on your record-keeping.

In addition to the abovementioned tip, here are a few more you can really use as a startup and moving forward:

Consult with a CPA

If you do not have an accounting background and possess little to no knowledge of accounting and accounting principles, you should consult with a Certified Public Accountant who will be able to advise you based on your business type and stance, on how to proceed. Be sure to inform them of all the important aspect of your business such as financing, loan notes, number of employees, theft protection, budgeting, etc. CPA’s are more expensive than bookkeepers, but they are better equipped to give pertinent advice and information for any business, because of their depth of study and experience. They will not be entering your transactions as a bookkeeper would; however, they will liaison with your bookkeeper or whoever is doing your bookkeeping to get the most effective system in place. Bookkeeping is necessary on an ongoing – often daily basis, but you can opt to engage a CPA on a quarterly basis and then at year-end in order to cut cost.

Small Business Development Corporation article “10 Questions to Ask Your Accountant” – questions you can ask your CPA within a couple of years.

Use software to handle your bookkeeping

Software is very convenient and versatile because they can do so much. Bookkeeping and accounting software are designed with bookkeeping and accounting in mind, and as such incorporate all the features that great bookkeeping and accounting require. You can of course use Microsoft’s Excel to enter your data; however, it will not be equipped to produce various reports about different aspects of your business as software such as Intuit’s QuickBooks would. In other words, documenting in Excel is better than not documenting at all, but using a system specifically designed for bookkeeping and accounting will yield better results in the short as well as long term. Your business may outgrow Excel, but it will not outgrow QuickBooks or Sage Peachtree for example. There is always the option of delegating or outsourcing your bookkeeping. You may have an employee upkeep your bookkeeping in your software system, or you can enlist an independent contractor or bookkeeping company to handle your bookkeeping remotely. I often recommend QuickBooks Online because it is so versatile, user-friendly, and convenient. You or your employee could be using it, at the same time your outsourced bookkeeper is making updates and reconciling.

Keep your business and personal matters separate

That starts with having separate bank and credit card accounts for your business that are used solely for business purposes. This will make it easier on your bookkeeping, saving you the headache of having to remember what transactions are personal vs business, and also allow your personal to stay personal in the event you are audited in the future. If you interchange business with personal and vice versa, and you have a business audit, you will be required to submit your personal information as well which can result in your personal being audited as well.

Setup an effective filing system and maintain it

A filing system is one of the most important components of any business. Invoices or sales receipts are going out and bills or purchases receipts are coming in, as well as purchase orders, estimates, statements, etc. In order to be able to access any of these, at any given time, they have to be stored in a designated place where anyone requiring them can retrieve them in a matter of seconds. There are several methods of filing system setup, but regardless of the one used, the important thing is to be able to locate whatever is needed at a moment’s notice. Customer Invoices does not need to be filed in paper form especially if they are done using a software and sent via email; however, bills and purchases receipts should either be scanned and filed on your computer or an alternate storage system, or be filed in paper form by date, vendor, or a reliable method of your choice. It is also critical to file bank and credit card statement together with their monthly reconciliation reports on a monthly basis, in a location where they can be easily retrieved. You will see as you go along the necessity of this.

Having a filing system and not maintaining it will absolutely defeat the purpose of having one in the first place. If files are removed for whatever purpose, they should be replaced as soon as they are through being used. If documents from the file need to be sent somewhere, it is advisable to make copies. This way you will not lose track of important paperwork.

Institute a sequential numbering system for Invoicing

If you are issuing invoices to your customers, there must be a way that both you and your customer can reference individual invoices. Applying numbers to your Invoices in sequence or order will facilitate easy tracking and follow up. I have seen this on quite a few occasions, and this is the epitome of error and confusion.

Access as much resources as you can – especially from your bank

If you are a “one man show” like many startup businesses, you can easily become burnt out and overwhelmed with the tasks that are not the core of your business, yet necessary and fundamental to having a fully functional business. In situations like this, simple things like having your bank attach copies of presented checks to your statements as well as give you detailed printouts of your deposits, could really take the edge off and make it more convenient for you when you are ready to enter or verify information. You can also ensure your bank facilitates downloads to software such as QuickBooks which can eliminate unnecessary time spent manually entering every single transactions. You will still need to review, but with only a couple clicking of the mouse, you can save up to four times the time it would take to enter it all. Using your bank’s “bill pay” feature is another great way to save time, as well as allow more detailed information to be downloaded from your bank. As a “one man show”, working smarter instead of harder will get you through more smoothly. Think about all the institutions you do business with and how best they may be of service to you, and use them.

Designate a specific area for your business – If home-based

If you work out of your home as many startup small business owners do today, create a distinctive space that is your business space. You can benefit greatly from this come tax time, but it is also crucial to have that space in the event of an audit. In addition, depending on the type of business you operate, you may have occasional customer visits and it will be much more professional to have a secluded designated area away from family distractions and disturbances.

Document business expenses incurred prior to your first day of business

Many businesses either borrow money from outside sources for their business startup or use their own funds as loan or investment. These incurred expenses need to be recorded regardless of the source, in order to have accurate books. If you borrow from an outside institution you will need to keep track of the amount so that you can make proper and on-time payment(s), and also record loan interest which is usually added to the principal loan – periodically. If you loan your own business money, you will need to record it, so that you will be able to repay yourself once the business starts making solid profit. For monies invested in your business, you should document for the same reason and especially to make your balance sheet more appealing in the event you require a loan in the future. Financial Loan Companies are more apt to grant loans to businesses that the owners have invested in. You may also be able to write-off some of the cost for that tax year, or have them depreciated over a number of years depending on the amount. For all these reasons, it is important to input incurred expenses in your financial recording.

Request a completed W9 Form from all eligible vendors

You are required to file 1099 Misc forms at the end of each year for all individuals, as well as businesses that are not Corporations, to whom you have paid $600 and upwards via a check. If you use other methods of payments such as debit card, credit card, Paypal, or other third party payment network, you should not report those payments or portions of payments as those agencies are required to report them on form 1099-K. The form W9 is to be fully completed with the vendor’s identifying number, address, and signature affixed. I am including this in the startup as I have seen how difficult it can be when trying to reach vendors at the end of the year when the forms are due to get this information, and how futile it turns out many times. Try and get this information as soon as you realize you will be making qualifying check payments to a vendor. It only takes a few minutes to complete this form, and it will save you the headache and extra effort put into locating them at year-end.

Generate proper payroll for employees instead of writing checks without payroll deductions

This is extremely important for businesses such as Daycare Centers where there is a requirement for a proportion of kids per adult supervision. If you are enrolled with twenty children for example, you cannot be the only caregiver, and must be reporting payroll deductions to the relevant authorities. Not having any payroll, or only yourself on payroll is a huge red flag and will most definitely summon an audit at some point. There are many payroll software on the market that you can use to get your payroll done, and also payroll companies such as ADP and Paychex that are designed to help small businesses pay their employees as well as remain compliant with tax agencies. Have your prospective employee(s) fully complete and sign form W4 which will ensure you have accurate information from which to setup their payroll account and make correct deductions and payroll. You must also file a new hire report with the relevant tax agencies in your State.

Starting your business is exciting, and there will be a number of core things to sort out and get through; however, in the rush to get your business off the ground, do not relegate your bookkeeping to the bottom of the “to-do” list. Find a way to incorporate it into your daily or weekly routine. Remember, there is always delegating or outsourcing! Not all tasks can be delegated or outsourced, but bookkeeping is one such task that most definitely can be. Start your business on the right footing, and continue in order to ensure its health, stability, and success.

Running a business can be exhausting, and many business owners find it very hard to delegate miniature tasks and let go – fully, of those tasks. Fully, meaning letting go of tasks and not the entire business; letting go of the task(s) given out to be done without hovering or hindering the process.

For example, I got a call a few days ago from a concerned small business owner on the upper east side of Manhattan saying that some of the transactions she is entering into QuickBooks is simply disappearing and nowhere to be found.

When I got there she opened the QuickBooks file in question, and indicated to me all the transactions she entered and where they should have been. I told her not to worry that I would find the transactions, especially because it is impossible for them to just vanish into thin air.

I have been using QuickBooks for such a long time that it did not take much time for me to realize that there had to be another file housing the “missing” transactions, and so I set out to view the other QuickBooks files that are on the Mac. She, however, proceeded to impede me from exiting the current QB file in question and from opening other QB files, constantly informing me that “none of those are the one in question, this is” which kept me from getting to the source of the problem and finding a solution. Within about 20 minutes of me just sitting there looking around the QB file that I know will not solve the issue, she was getting very frustrated saying, “I told you they are nowhere to be found, you cannot solve it!” She then started pacing, and taking phone calls and during her brief episodes of distractions I was able to look at the files in date order to determine the latest ones used.

The problem was just as I thought!

She was using three different QB files to enter her data, and of course there were like 10 transactions in one file, then the next 17 in another, and another 38 in the next. She was using a Mac and it is very easy for a situation like this to happen because of the way QuickBooks for Mac works. Unlike the PC versions, each time QuickBooks is backed up on a Mac, it creates a different backup file with a “Disk Image”. This makes it particularly easy to use a different QB file each time an update is done, without actually noticing until you really need to. That is one very big difference between the Mac and PC versions of QuickBooks.

I then summoned her over to the computer, showed her the “missing” transactions in question, and explained to her what was happening. She was ecstatic, and of course I was happy too that I had solved the “huge” problem she thought no one could, but I had to bring it to her attention that if she was there redirecting me each time I try to do what I am best at, the problem would not have been solved. What could have, and would have taken me a few minutes, ended up taking over an hour.

My point to small business owners or any person seeking assistance, is to give professionals in fields you do not specialize, a little room to do what needs to be done to help the particular situation. You can sit and watch, especially in instances where you feel your privacy could be breached; however, do refrain from directing a process you are not knowledgeable about – one you have sought help for. Think about it, if you could have solved it, you would!

Many small business owners find it easier or more convenient to use independent contractors than to hire employees; but is the arrangement you have with a worker that of an independent contractor or that of an employee?

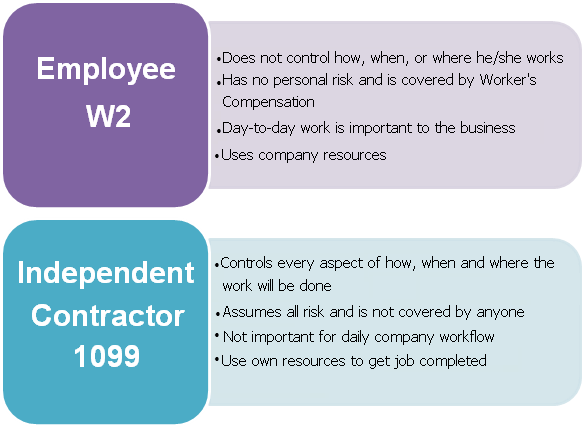

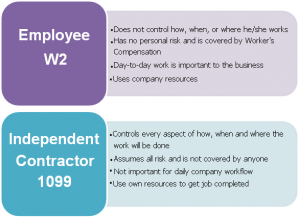

According to the IRS, there is a huge difference between an employee and an independent contractor, and they are adamant about doing all they can to ensure each is treated as who they really are by every organization. So how do they expect you to differentiate and treat each? Below are a number of key questions, based on IRS Guidelines, that when answered will lead you to the most suitable solution for your particular situation of who your worker should be – an employee or an independent contractor:

How often does this person work for you? How regularly someone works for you is more important than how many hours they work for you. For example, an accountant who balances the books on a quarterly basis is definitely not an employee as is an assistant who comes in once per week on any day chosen by her, to catch up on the previous week.

Do you set the person’s schedule? A key indicator of employment status is how much control you have and exercise over a worker’s schedule. Independent contractors set their own schedule, employees do not.

Do you instruct or supervise the worker? While you are probably providing all workers with some guidance, how much control you have over their approach helps determine their status. Independent contractors listens to what you want to get done, but use their own approach to get it done. Employees are often told what, how, and when to do what.

If additional workers are needed for a job, who hires them? The amount of control you have over a worker’s decision-making power is an important factor in determining their employment or non-employment status. Independent contractors are responsible to get the task they are given done and to hire help if they need to. Employees do not hire additional help, their employers do.

Who provides the tools and materials necessary to complete the job? Employees use the company’s equipment and supplies; independent contractors provide their own.

How is the worker paid? The timing and method of payment are important indicators of worker status. Employees are often on payroll, whereas independent contractors invoice for payment. If the person is paid regularly, he is most likely an employee. However, those who are paid only when a project is complete, or a sale is made, may be an independent contractor. (A bit blurry, but looking at the entire picture will dim the blur.)

Do you reimburse this worker for any business or travel expenses? Companies generally reimburse employees for expenses, while independent contractors pay their own to get the job or task complete and will add all expenses to their Invoice.

Can this worker’s decisions impact their own profits or losses? Independent contractors generally take on a degree of financial risk that employees do not. Renting an office, maintaining equipment, advertising and having multiple clients can all indicate profit-or-loss risk. Employees are risk free and are also covered with workers’ compensation.

Is this person hired to work indefinitely, or for a specific project or time period? How long someone works for you is one of the key considerations in determining employee status. Someone who works indefinitely is “probably” an employee. Someone who works on specific project or for a fixed time period may be an independent contractor. (This is where the lines start blurring for me.) If someone is working for me once per year and I want to have them working for me until I am out of business or he quits, then this person definitely does not sound like an employee to me even though he is working with me indefinitely. But again, looking at the big picture will minimize this blur.

Are the person’s activities essential to your day-to-day business? The role a person plays in your broader business is a critical factor. If someone has to keep the business pumping such as a receptionist at a hotel, or a chef at a restaurant, then of course they are employees.

In short, if:

You the employer control how, when, and where this person works, this worker is an employee.

This person takes little or no personal financial risk, this worker is an employee.

This person’s work is relatively important to your business, this worker is an employee.

This person uses your resources – computer, printer, office supplies, etc., this worker is an employee.

The IRS has got to be one of the most complicated entities around. Nothing is ever black or white and the gray area seems to be endless. Yet, we all have to ensure we are in compliance with their many rules and regulations at all times. For this reason, it is usually a great idea to consult with a tax or legal advisor before deciding on any factor as it relates to the government taxing agencies.

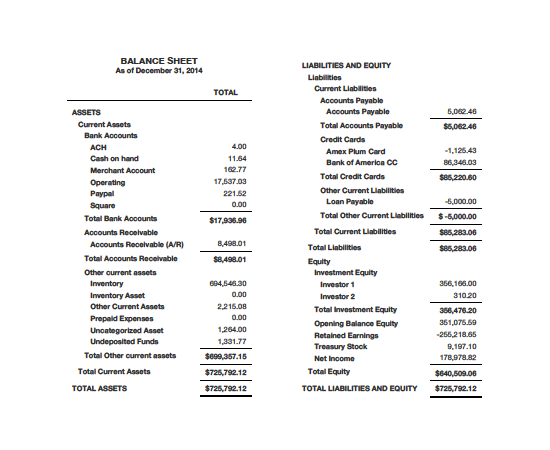

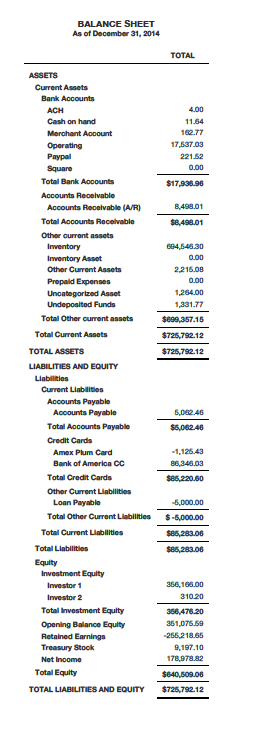

The Balance Sheet is an important report in your financial statements that shows the ending balances of what you own, what you owe, and how much you have invested in your business since its inception, as at a particular date. It is divided into three (3) main categories:

Assets

Liabilities

Equities

1) Assets – What You Own

Balance sheets usually start with cash balances that include monies presently in your bank account(s) as well as your petty cash till, minus checks you may have written but are not yet presented to your bank to be cashed. Those outstanding checks would reduce your account balance(s) once they are cashed. Monies in your Paypal, Square or any other ecommerce portals that allow you to receive payments are also shown in this section of your balance sheet.

If customers owe you money that you have invoiced for but not yet received, you will see those outstanding amounts in Accounts Receivable on your balance sheet.

If you sell products, the cost of all of them that you have purchased and not yet sold will be in the Inventory Asset account.

If you own equipment, furniture, vehicle or something similar that lasts for years, you will have a balance in Fixed Assets for what you paid for these items. If it has been a while since you have owned them, you may have a Depreciation account, and when you net the two, your Fixed Asset values are reduced.

All of the above are assets and they are listed in the first section of a balance sheet.

2) Liabilities – What You Owe

If you owe money for taxes, to vendors, or to employees, then it will show in the Liabilities section, which is the second of three major sections of a balance sheet. Day to day unpaid bills are in an account called Accounts Payable, and separate accounts are usually set up to document monies owing for taxes, etc.

If you have bank loans, they usually each have a separate account like a bank account does. Each bank loan account represents the principal due on a loan (the interest you pay is recorded in the expense section of the P & L).

3) Equities – All Monies You have Invested In Your Business Plus/Minus Its Income or Loss

The final section of the balance sheet is the Owner Equities. It is the section that will vary the most depending on the type of entity your business is set up as. For example, if your business is a corporation, there will be a common stock account that will represent the original amount of money you put into the business. It will match the Articles of Incorporation that you drew up when you incorporated. This amount will rarely ever change for the life of the business.

Also, there is usually an account called Paid-in Capital which is how much additional money you have put in or taken out of the company beyond the common stock balance.

A corporation will also have a Retained Earnings account. This reflects accumulated profit (or loss) through the years of operation.

If your business is set up as a partnership, the equity section will include an account for each partner that represents their balance in the firm, which is the net amount of money they have put into the business over the years minus the amount they have withdrawn as well as plus or minus the business income or loss through the years.

Unlike the Profit and Loss or Income Statement accounts that are zeroed out at the end of each accounting period, the balance sheet accounts accumulate continuously and does not clear out at the end of each accounting period or year. Thus, the P & L or Income Statement report can be generated using specified date range while the Balance Sheet report can only be generated as at a particular ending date and not by range of dates.

There is always room for improvement, and what better time to take stock, analyze, and set in motion the changes necessary to facilitate improvement than at the beginning of a new year. Here are five surefire things you can do to launch your business to new heights.

Afford Your Business a Website (With a Blog)

Formulate a better relationship with your Customers or establish one

Gain New Customers by Marketing to Your Target Prospects

Know your business trend. Know your numbers.

Delegate tasks you do not do well, or enjoy doing

1) Afford Your Business a Website (With a Blog)

Your business is doing extremely well and you do not have a website. Awesome! Kudos to you! But guess what, there is always room for improvement, and your business can still do better. A business without a website and a blog is like an unpublished book; you have it but no one knows about it.

Unless you are Walmart, Staples, Home Depot or any other well established brand, operating a business without a website and a blog is futile if generating leads and having conversions is your goal for your business. The Internet is the number one place people turn to for information whenever they need to, and if you are not there you will not be found in their search results – even though your product and/or services may well be what they are looking for. You are missing out on the competitive edge! Adding a blog to your website is the best way to increase traffic to your website so more people can know about you and your services. The more visitors you get, the more leads you can generate. And the more leads you generate, the more business you will close.

Write quality content

Of course, you need to write content that people will actually be interested in and want to read! Your goal here is to get publicity and ultimately gain conversions, but in order to gain more high quality leads you will need to put some quality time and effort into your blog construction and presentation. Write articles relative to your business on a regular basis and publish them. They do not have to be long and winding; quality over quantity is king any day! Don’t just slop something up in two minutes and call it a post, if you do not have time to write a decent post, don’t post anything at all. A bad, sloppy post can actually do your business more harm than good. Your blog represents you and your brand, so put some thought into what you publish. As Melinda Emerson the Small Biz Lady warns, “There’s no separating you from your business, and you have to brand yourself accordingly.“

Promote Your Blog Posts

Now what purpose would it serve if you put all that effort into writing content that you think will be just what your prospects want, if you do nothing after writing them and hitting the publish button. None whatsoever! You must promote your blog content to social media sites, which is the only way anyone will know they are available and be able to read them. Apps, such as HootSuite, is a useful tool that allows you to manage multiple social media network accounts in one easy to use interface. You can schedule updates ahead of time, and publish across platforms at once, which is very convenient as it gets the word out on many platforms with minimal time and effort. With only 24 hours in a day, it is critical to make every minute count.

2) Formulate a better relationship with your Customers or establish one

Yes, you may have employees who are designated to various positions having direct contact with your customers, but in taking your business to the next level, you must periodically reach out to your customers and make a direct connection. There is a difference when a customer hears from a business owner than an employee. Connecting directly shows that they are valued, which puts you at an advantage where you can also gain valuable insight that can help enhance your business’ bottom line. This may not be practical for large companies with a broader customer base; however, they can devise an effective customer support team that will provide their customers with the best customer service possible. Your customers will let you know how satisfied or dissatisfied they are, at which point you can get to the drawing board and aim to please the disgruntled. As humans, we are built to want better, and as such we are always looking for ways to improve. Your customers are no different! They want the best customer service as well as the best product and service for their dollar, and will not hesitate to look elsewhere.

3) Gain New Customers by Marketing to Your Target Prospects

It has been said time and time again, and cannot be reiterated enough, how important it is to: 1) have a niche market, 2) know your target audience, and 3) develop strategies geared towards them. Marketing is a must if any business is to succeed. If done right, it will yield favorable but if done wrong, you will waste valuable time yielding zero results. Have a niche market so you know whom you are targeting. For example, if you are marketing to college students, you will have an idea of what to include in your marketing material, where to market, and when to promote your goods or services. Stop wasting valuable time and resources marketing to everyone, and cater to your target audience.

4) Know your business trend. Know your numbers.

Many small businesses that have closed their doors could have been around today had they kept score of their business’ numbers on a regular basis. They consistently operated at a loss, with minimal to non-existent cash flow, and yet failed to keep score of their daily, weekly, or at the very least – their monthly numbers. You should be improving, not declining. Keeping score of your numbers will allow for early intervention where you can identify areas that you can make improvement on and areas you can eliminate. Know what is taking place in your business with your business finances. Pay attention to your financials! Even though you may designate certain financial aspects of your business to enable seamless operation especially when you are unavailable, you should find a way to know that what should be happening is actually happening, and nothing more or less. You must have a firm understanding of your cash position every day, which can be accomplished by carefully managing and monitoring your banking relationship, and your books. Also, does your business require more funding at certain times of the year than others? Do you usually have down-time at certain times during the year? What will you be doing during that time? And, how will you maintain your business paying those overhead costs? These are some of the questions you should be able to answer at any given time.

5) Delegate tasks you do not do well, or enjoy doing

Even as a small business owner, there will be areas of the business that must be taken care of that is either not in your scope of knowledge or a part you enjoy doing. The latter will drain you emotionally and physically, and may even put a damper in your passion for your business. We are living in an era of technological advancement with software and information everywhere, and as such, many business owners looking to save on cash, are attempting to do it all by themselves, even without the skill base necessary. But mistakes can be costly, and in many cases there is only a very slim margin for error. You know your organization best, as well as your capabilities. Don’t waste valuable time mulling over subordinate or mundane tasks that you could otherwise designate! Take stock and delegate the tasks that are weighing you and your business down, and prepare to soar.

Implement the above-mentioned five changes and and watch your business flourish in an upward chain of improvement.

What are your thoughts? Feel free to express in the comment section below.

Employees are valuable resources who are not only equipped with the expertise and knowledge for the role you initially employ them, but they also house talents they have harnessed and skills they have honed which you may not be aware of, unless you tap into them. This may not apply to all your employees; however, if you do not utilize the opportunity of tapping into them you could miss out on possible skills and information that could take your business to the next level. Whether you own a Fortune 500 Company or a “Mr. Jay” corner store, perceiving and engaging your employees as a means of resource and not mere commodity, can exponentially benefit your business.

I have witnessed firsthand where employees go from nonchalant to concerned, activated employees. For many employees, their only reason for going to the job is merely the paycheck. They have zero interest in the company and as such very lackadaisical, and this outlook sets the tone for unhealthy customer service, stifled employee relations, an unmotivated work environment, and a stagnant or declining business. This is not a situation any business owner would like their business to be a part of, and thankfully, there are ways to not only energize your employees, but also connect them to your business strategies.

5 Step Approach To Utilizing Employees Full Potential

Activating and mobilizing your employees

Creating and implementing strategies that are geared towards business success with a theme of employee involvement

Empowering your employees

Opening and aligning the channels of communication

Re-examining protocols and promoting continued collaboration

Step 1. Activating and Mobilizing Employees

You activate and mobilize your employees by giving them a voice, clear roles to play, and incentives. Studies have shown that humans are more likely to be attentive and receptive when rewards are in play. Essentially, in order to boost employees interest you can offer incentives for participation in both internal as well as external surveys. Surveys can range from individuals view of operation to customer satisfaction, as well as their social group stance on matters that are important to the particular business.

Shift your thinking to inspire your employees to be active in something that is about them. Give your employees business cards. Employees will start to feel like a part of the organization and not just a commodity for the company, and this will solidify their new stance of the business, and activate a drive to see the business succeed. Each time they hand out their business cards, your company gains new prospects who could quite possibly convert to new customers. Your equipping them with business cards allow them to market your business indirectly, while having a sense of pride. Employee activation is just as important as traditional external consumer-focused efforts. More than a paycheck, employees desire a sense of purpose, pride, and impact.

Step 2. Implementing programs and surveys and directly Connecting Your Employees to Your Business Strategies

After you have clearly conveyed your company’s purpose to your employees, you can start implementing programs that links them to your business strategies:

Host brainstorming sessions and allow your employees to participate. Bringing together different perspectives harmoniously is important to leveraging individuals’ collective talents.

Invite them to write articles for company blog. You can rest assured they will be broadcasting to their social networks the awesome work they are doing contributing to their company who values their input, which in turn converts to indirect marketing for your business.

Create monthly or quarterly internal newsletters showcasing how your employees have helped to improve the company over a period, and putting forth additional plans for impending months. Also, communicate upcoming opportunities to your employees in your newsletters, as well as in a face-to-face meeting setting.

Implement a mentorship program that allows seasoned employees to mentor newly hired ones. This will again give them a sense of purpose to the company, and show that you trust and value them. You can create a template they should follow and give them space to test their own learning methods.

Step 3. Employee Empowerment: You Can, and I Trust You To

Employees desire to feel appreciated and valued. When employees are involved in the equation, they will feel respected and as such exude a sense of loyalty and care for the organization. Consulting with employees help to promote a healthy working environment where all involved in the organization can benefit. Employees are in the everyday happenings of the company and as such, experience issues firsthand concerning customer relations for retail businesses, as well as internal controls that affect the organization. Without co-operation between employers and employees the chances of coordinating a successful healthy business is non-existent. In addition to empowering your employees with confidence and trust, you can create programs that advance them professionally, and subsequently give them room to implement strategies learned. As business owners, we all have to ensure we are offering learning and development opportunities on the job, and challenges to promote growth.

Step 4. Communicating Effectively: Speaking With, In Lieu of Speaking To

Effective communication is essential for the smooth running of the organization; communication that is not one-sided, but all-inclusive and understandable. As one great writer wrote, “The single biggest problem in communication is the illusion that it has taken place.” We cannot assume communication has taken place, and in order to ensure it has, all parties must be attentively involved in the process and in a reciprocative manner. When you speak to someone, you do not listen. On the other hand, when you speak with someone you speak as well as listen which is effective communication. Also, as business owners, it is imperative to make one-on-one time to speak with employees to find out what is on their minds. Do they have ideas for improving the business, or ways to promote a better workplace? What do they want to accomplish professionally? When employees feel the company is responsive to their concerns, and values their input, their desire to participate and contribute increases substantially. Improving interactions among employees as well as with management will strengthen morale, build team spirit, increase productivity, and create a cohesive, motivated workforce.

Step 5. Re-examining protocols and promoting continued collaboration

Based on company’s performance over a quarterly, biennially, or annual period, and employees feedback, reexamine issues affecting the company that can be changed and areas that can be improved. Foster a community of committed employees, and take all the steps necessary to promote continuous collaboration, and avoid complacency.

Setting an operational plan without consultation with employees disadvantages the organization because: 1) Lack of consultation fails to take advantage of all available knowledge and expertise and 2) Lack of consultation is most likely to make people feel left out which sets the tone for reluctance and negativity towards the emerging plan. Because employees are on the front line, they will affect the core of your business – your customers. Given the right atmosphere in which they feel valued and needed, they will exude confidence in their ability and it will shine through to the customers. What you will have is an employee-driven workplace with revitalized employees geared towards enhancing your company’s growth and development – collectively.

Your employees can make all the difference when it comes to growing your company. They produce, deliver, and manage your products and services day in, day out. This is why your HR strategy should include opportunities for training and recognition programs that keep your employees stimulated, strategic employees involvement programs, and clear cut communication channels which will all work together to keep your company thriving. Employees are really a reservoir of resource. Tap into them and watch your business grow.

What are your thoughts? Feel free to express in the comment section below.

Use the Right Accounting System

Use the Right Accounting System

Create a

Create a  Enter all transactions that have taken place since the beginning of the year in your accounting software, or on your excel sheet, if you are a spreadsheet user. I do not recommend spreadsheets be used as your main bookkeeping tool, as it is very limiting, and allows for more mistakes to occur. However, if your CPA or tax preparer has been and continue to accept your spreadsheets without complaints, then you should probably continue to use them. On the other hand, if your CPA or tax preparer has been ignoring you and not preparing your taxes on time after you have submitted your spreadsheet info, you can opt to use one of the many accounting software available on the market for desktop as well as online or “in the cloud”. Some of them will tell you to have a bookkeeper crunch your numbers, but others will push yours aside, and work on their clients with accounting-software-prepared reports first. Accounting software are more versatile, and you are able to generate all the relevant reports that a CPA or tax preparer requires. Also, reconciliation is one of the most important steps in keeping accurate books, and while it is possible with spreadsheets, it is more convenient and less error prone when done using accounting software.

Enter all transactions that have taken place since the beginning of the year in your accounting software, or on your excel sheet, if you are a spreadsheet user. I do not recommend spreadsheets be used as your main bookkeeping tool, as it is very limiting, and allows for more mistakes to occur. However, if your CPA or tax preparer has been and continue to accept your spreadsheets without complaints, then you should probably continue to use them. On the other hand, if your CPA or tax preparer has been ignoring you and not preparing your taxes on time after you have submitted your spreadsheet info, you can opt to use one of the many accounting software available on the market for desktop as well as online or “in the cloud”. Some of them will tell you to have a bookkeeper crunch your numbers, but others will push yours aside, and work on their clients with accounting-software-prepared reports first. Accounting software are more versatile, and you are able to generate all the relevant reports that a CPA or tax preparer requires. Also, reconciliation is one of the most important steps in keeping accurate books, and while it is possible with spreadsheets, it is more convenient and less error prone when done using accounting software. Reconcile your bank and credit card accounts from the start of the year to date, so you will not be backed up and out of synch at year end. It is always advisable to reconcile your accounts on a monthly basis, not only to stay updated, but especially to ensure there are no mistakes on either side, and if there are, to catch and resolve them immediately. Reconciliation ensures that the bank and credit card numbers are in synch with your numbers; as such, you must keep a record of all your transactions, and reconcile them against your bank and credit card statements. Humans are prone to err and so are credit card companies and banks.