Photo courtesy of APO Bookkeeping

For any number of reasons, you may opt to do your bookkeeping on your own instead of hiring a bookkeeper in-house or outsourcing your bookkeeping. Like many things, there are advantages and disadvantages to doing your own bookkeeping, but with some basic accounting knowledge and a keen eye for detail you should be able to pull it off. Here are a few tips to help you as you do it on your own:

Use the Right Accounting System

Use the Right Accounting System

Accounting is either cash-based, or accrual-based. With the cash method, you count the income when you receive it, and expenses when you pay them. Under the accrual method, you count income and expenses when they happen, and not when you actually receive or pay them – respectively. The other main difference between the two methods is the ability to budget accurately. Accrual method of accounting allows for better budgeting and planning because it looks at when liabilities are incurred and revenue earned and not when cash is paid. This method puts on the books liabilities that might otherwise be forgotten, like accrued interest. The cash method does not take accrued interest into account until it is required to be paid. This could put a strain on a small business that did not plan to pay out accrued interest balance, and is now faced with cutting expenses in other areas to have enough cash to pay the outstanding balance. The two methods have their advantages as well as disadvantages, and as far as filing taxes, the IRS only requirement is that you use the accrual-based system if your annual sales is more than $5 million or you store inventory.

Record transactions as soon as they occur

If you are using spreadsheets for your bookkeeping, or doing it manually on paper, you need to record your transactions as soon as they occur. If you are using an accounting software such as QuickBooks, you need to decide whether you will be recording transactions as they happen or adding them via the bank downloads later. Regardless of the method you use, keep your books updated at all times. Doing so will allow for little to no discrepancies, better workflow, and you will also have updated information on which to rely for decision making.

Record all business transactions

In order to have accurate numbers from which to make good business decisions, and file correct tax returns, you need to ensure all numbers affecting the business is accounted for and recorded. For example, if you are a business owner who sometimes uses personal funds for business expenses – and vice versa, you need to include those numbers in your bottom line.

Track Reimbursable Expenses

As a Small Business owner, it is very likely to sometimes use your personal funds to for pay business expenses. These monies should be reimbursed to you as well as recorded in the company’s expenses, and so there should be an account created to keep track of these reimbursables. Also, if your employees are construction workers or engineers who are usually in the fields and may use their funds to make small purchases that are immediately needed in order to continue their work, you need to collect those receipts and add them to the reimbursable account from which you will later repay them. Doing this is also important for accurate job costing.

Keep Accounts Categorization Simple

Overcategorization leads to miscategorization and ultimately inaccurate reporting. As a small business, you should be able to categorize your accounts in three to four sections:

1) Income – under which you can create subaccounts of your various streams of income

2) Cost of Goods Sold or Cost of Sales – under which you can create sub accounts for the employees salaries who are directly involved in the creation of the products you sell or the services you offer, as well as the products purchased to be used in the creation of your complete product for sale.

3) Operating Expenses – under which you can create a subaccount for Administrative Expenses and further subaccounts under Administrative expenses to list those individual accounts.

4) Other Expenses – under which you can create subaccounts to list other expenses that do not fall under any of the above categories.

The balance sheet accounts are usually fairly standard with three main sections: 1) Assets, 2) Liabilities, and 3) Equity each with their own subaccounts. You will need to create additional accounts on as needed basis. For example, if you loan money to your company, you will need to create a liability account to record these amounts the company owes you. Likewise if you borrow money from your company, you will need to create an asset account to reflect this.

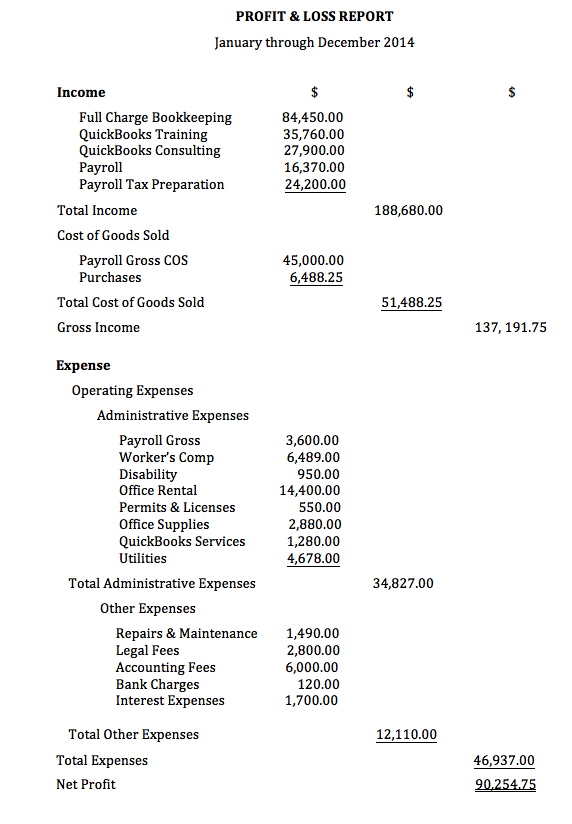

Here is an example of a Simple Profit & Loss Report or Income Statement:

Deduct Sales Tax from Total Sales

If you are a retail business that collect sales tax on behalf of the government, you should deduct these sales taxes from your sales. If you are using a software such as QuickBooks for your bookkeeping, and you do not track inventory in QuickBooks, you can setup this account as an Income account and set it as a discount so that it will be listed at the top of your Profit and Loss report and lessen from the total sales. Also, avoid penalties and interests and pay over your sales taxes as soon as they are due.

Keep Proper Records of Loans Received

Many small business owners need financial backing at their startup, and may take out a loan or two. These loans must be recorded and tracked in separate accounts, paying special attention to separating the principal repayment and the interest payment. The interest is an expense to your company and should be recorded in the expense section of your income statement or profit and loss report, while the principal is made towards your loan balance which will be in your liability section of your balance sheet.

Use Checks or Credit/Debit Cards Instead of Cash

Cash makes it harder to keep track of spending. Misplaced receipts, forgetting to document purchases all can be avoided if checks or debit/credit card payments are made. Not only will you have the amounts available to record, but you will also have details on uses of funds.

Reconcile all Business Bank & Credit Card accounts every month

This is one of the best business practices to employ! Reconciliation is a fundamental aspect of bookkeeping. Not only will you be able to catch any mishaps that occur; it will spread your workload and keep your books up-to-date-and accurate. Also, any mistakes on the bank’s or credit card company’s part that are not caught within six months, will not be able to be resolved. If you look on your statements, you will see that the banks include a reconciliation sheet and recommends that you reconcile your numbers with theirs. Reconciliation is the only way to ensure your numbers are accurate and your bookkeeping on par.

Let Payroll Specialists Handle Your Payroll

Payroll and payroll taxes can be complicated/intricate and not only do you need to ensure your employees paychecks are precise, but you must make correct payroll deposits as well as file accurate taxes. Payroll specialists are trained especially for this, and so they know the ins and outs, and are fully equipped to get this done accurately.

Keep a Proper Filing System in place

Not only is this good business practice, but you do not want to drive yourself crazy trying to find one document that is urgently needed – pronto. As a “do-it-yourselfer” it will greatly benefit you to keep a proper filing system where you will file all documents and paperwork in a manner that makes them easily retrievable.

Keep an Eye on Your Cash Flow

Cash is King for any business, and the lack of it is the reason so many small businesses fail. Know how much it takes to keep your business running on a monthly basis! Devise an accurate system of expenses and monthly obligations, and weigh them against your reliable monthly inflow of cash. Include an extra 20% of total expenses to your expenses for a bit of “cushion”. A budget and forecast report is a huge plus to create, maintain, and use as a financial guide.

Give Your Customers Options to Pay You

Providing your customers with a variety of payment options will not only make your customers happy as far as convenience, but it will allow you to get paid more quickly. In today’s fast paced world, convenience goes a long way! Some customers may procrastinate writing that check AND mailing it, or setting up that online bill pay. Allowing them the option to pay you via your submitted invoices will be a huge plus in helping your cash flow.

Invoice Customers on Time

The sooner you bill your customers the sooner you will get paid, and that will also help keep your cash flow up and your budget on track.

Pay Bills on Time

Pay attention to those vendors who are sacking a late payment fee to late payers. Take advantage of those terms of payments you get, but make every effort to meet them. The delay will help with your cash flow, but may accrue interest if not paid on time.

Have your vendors submit a completed and signed W9 form

For vendors to whom you have paid a minimum of $600 and above during the year who are not a corporation, you will need to report their payments to the IRS on from 1099-Misc at the end of the year. You will need specific information from them to include on this form such as their mailing address and tax identification number. It is best to keep W9 forms on hand, so that you can have your vendors complete them at the time you realize that the monies you are paying them are at this threshold. You should check your vendor balances to see if the monies you have paid them are amounting to $600 and above, as you may often write a check for under six hundred but may make more payments to them amounting to $600 and above throughout the entire year. Waiting for year-end to collect this information may be a daunting task, which many times – from my experience, has proven futile. You cannot file form 1099 without the vendors tax identification numbers, and of course you will need to mail their copies to them. If you pay your vendors through a Payment Portal such as Paypal or with your credit card, you will not be required to file or include those amounts on your 1099 as these companies are already reporting them on their 1099k.

Backup Your Computerized Information

Computerized systems as well as software do fail at times, and it would be devastating if all the work you have put in to your system were to become corrupt beyond repair, or inaccessible. Portable Hard Drives like this Toshiba Canvio Connect II 1TB Portable Hard Drive or this Seagate Backup Plus Slim 2TB Portable External Hard Drive with Mobile Device Backup USB 3.0

will store a copy of your information for easy retrieval, and save you the headache of ever losing your information that you have worked so hard at compiling.

Leave an Audit Trail

If you have a system that allows you to quickly and easily retrace your company’s financial activities, your record keeping is effective. This includes keeping your invoices and checks in numeric order, not skipping check or invoice numbers, and keeping bank and credit card accounts separate. You should be able to retrace a year or years and have a clear trail of your company’s financial activities.

The best way to work as a “do it yourselfer” and not be overwhelmed, is to always keep every area of the business up-to-date. Designate a time to get the tasks that can be done later such as recording reimbursables and paying bills, and do the ones that cannot wait – such as Invoicing and attending to your customers first. Create a monthly chart with a daily workflow that you will be able to model everyday, and stick with it.

Eugénie, very useful tips you have listed here, thanks! I’ve been doing my own bookkeeping up until this point; however, it’s sometimes difficult to manage all the various aspects of my business and my books don’t always get reconciled each month. The thing is, I need help! Period. But, I am not too keen on handing over my bookkeeping to an employee. How does outsourcing work with you? How would I get my info to you? And, how would we collaborate? I use QuickBooks Online so we should both be able to use it at the same time. Look forward to seeing how it could all possibly work. Thanks in advance!

Hi Janice, yes it can definitely be a handful to manage all aspects of a business, and do so effectively. Reconciliation is super important, and it should really get done monthly. So yes, Janice! You need help! And I’m delighted that you came to APO for that help. A few of my clients have this same issue, and I do understand you wanting to keep your financials entirely private from your employees. Outsourcing your bookkeeping with us is pretty simple. You would send us your statements, and all other information that are relevant to getting your bookkeeping done via our secure upload, or you could email them if you prefer. You would also send us an invitation to connect to your QuickBooks Online file, where we will create our user ID and password to login. You will be able to see everything that I am doing in your QuickBooks vs what you are doing in QuickBooks, which is pretty cool. It is also great that you are using QuickBooks Online, because it allows multiple individuals to work in it at once, which is really good especially if you use it daily for Invoicing and sales. We update and reconcile your QuickBooks on a monthly basis, ensuring it is always current. We will communicate with you at regular intervals with questions we have or concerns that may be revealed. Here is our contact info APO Contact, feel free to send a more detailed email with your contact info. so we can begin collaborating. Thanks Janice!

Yes, it’s almost that time of year again for 1099’s! Your tip definitely helped me last year Eugénie, and I have instituted your very important tip to never pay a “qualified” vendor without first having them complete the form W9. This works wonders! Prior to implementing this, it was a headache trying to get their tax info at year end. Thank you so much for offering this value to us!

Hi Katherine, my pleasure! Yes indeed, it’s 1099 time! Happy you are finding value here. All the very best!

Real, usable tips as usual Eugénie, thank you!

I have this class issue and I’m not quite sure how to solve it. I use the class feature to track my transactions for the various accounts, but I sometimes forget to assign the classes. Is there a way to see what transactions are not classified? I’m afraid the reports will give me incorrect numbers if I don’t get this right.

Hi John, thank you! So kind! I take it you are using QuickBooks; if so, then yes, there is a way to see the transactions that are unclassified. From the Reports menu in the desktop editions of QuickBooks, go to Company & Financial then Profit & Loss by Class and change the date to “All” or the particular period you need. The classes will be listed in columns and there will be one for unclassified – if you have transactions that are not yet classified. Click on each amount in the reports to edit those transactions and assign to their respective classes. Next, go to Reports > Company & Financial > Balance Sheet Detail and use the “filter” option to filter the report by class. If you are using QuickBooks Online, go to Reports in left menu bar, type Profit and Loss in the search field and select it from the list. Next, click Customize at top right of screen, then Filter and check the box to the left of Class. Now, ensure the date range is correct for the period you are checking, then click Run report. Do the same for the Balance Sheet Detail in QuickBooks Online. Your reports by class will definitely be incorrect John, if transactions that relate to those classes are not classified. Hope this helps!