Photo courtesy of APO Bookkeeping

Managing your accounts receivable is very important because the timing of receivables plays a major role in your company’s cash flow. In addition, you want to ensure your customer balances are accurate, and your receivables current, based on the terms of service you offered your customers. Reconciling the individual customer account balances with the general ledger balance establishes the accuracy of the balance sheet asset. Reconciliation of your receivables should be done on a monthly basis – at least, as part of the month-end closing process.

What is Accounts Receivable?

Accounts receivable is the monies your customers owe you which is derived from the goods or services you have sold them or provided for them – respectively, on credit. When you sell goods or services to your customers on credit, the amounts they owe your business make up the accounts receivable balance in an accounting record called the general ledger. Their individual balances are found in the subsidiary sales ledger and listed in the aged accounts receivable report. This aged accounts receivable report will keep you apprised of the monies that are due, so you can reach out to those customers before they become way overdue. Reconciling accounts receivable means you are ensuring that the total of the individual amounts due from debtors equals the balance of the accounts receivable account in the general ledger.

How is Accounts Receivable Reconciliation Done?

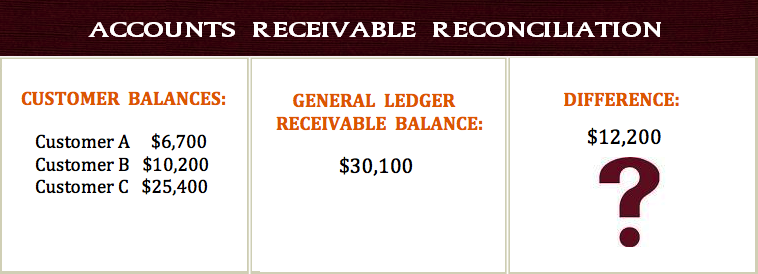

You need to verify the general ledger accounts receivable balance, starting with the balance brought forward from the previous period. To do this: 1) Add the total of all invoices issued from the sales day book and deduct any credit memos issued. 2) Deduct the total payments received from customers – taking the figure from the cash book, and add any finance charges made. (If you post open credits (overpayments or advance payments from customers) to a separate general ledger account, the total at this point should be the same as the accounts receivable balance.) 3) Deduct open credits and add open credit refunds. 4) Check the final figure against the total of individual customer balances from the aged accounts receivable report. Any difference between the two balances must be investigated.

Common Reasons for Discrepancies in Accounts Receivable Reconciliation

The most common reason for discrepancies in accounts receivable reconciliation are journal or adjusting entries made directly in the general ledger and not reflected in the subsidiary sales ledger, or vice versa, and differing cutoff dates of the reports used. Two other possible reasons for discrepancies in the reconciliation numbers are; incorrectly offsetting customer and supplier contra-accounts, and posting to the wrong general ledger account.

When you have identified all the errors, you need to make the adjusting entries needed for the accounts to reconcile with the correct balances, and include a clear description of the reason for each transaction for auditing purposes. Where possible, reverse the incorrect entry and re-post it correctly, rather than posting the difference only, to make the transaction easier to follow. When all entries have been made, reconcile the balances again as a final check.

Incorrect accounts receivable balances will not only throw off your business financials as far as the receivables showing more monies owing than are actually owing, or vice versa, but can also make you lose valuable customers if you repeatedly send them statements with inaccurate balances. One time? May be not so much, but more than once could shout incompetent or dishonest.