by Eugénie M. Nugent | Jan 5, 2017 | Business Improvement, Business Tips, Financial Reports

Photo courtesy of APO Bookkeeping

There is so much you can get from Excel spreadsheets, and no more! Don’t get me wrong, Microsoft’s Excel has its many purposes one of which is capturing information and making calculations including statistics with useful bars and graphs resulting in eye-catching, aesthetic presentations; however, it does not have the capacity to convert information from one report type to another, reconcile entries, or provide real-time bookkeeping and accounting stats, and therefore cannot provide the cross-reporting intelligence analysis that businesses need in order to facilitate strategic planning and make good business decisions. It is not enough to know how much profit has been made thus far for the current year, or how much your current expenses are; businesses must be able to look comprehensively at their business stance at any given moment, if being successful and staying in business for the long haul is their main goal.

Use an Integrated Financial Solution Software for All Your Business Accounting Needs

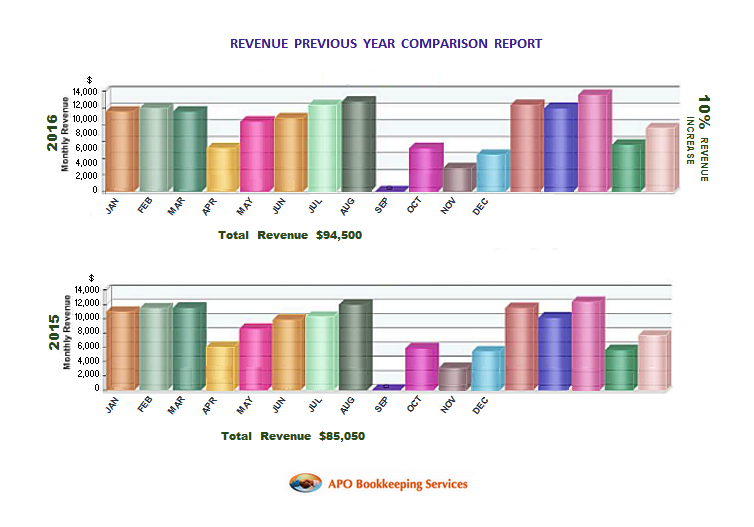

This is where cross-reporting, intuitive, integrated financial solutions software such as Intuit’s Software – QuickBooks, and Sage Peachtree come in. With an integrated financial solutions software, you enter the information once, and you get to use that same information in a variety of ways to pull insightful reports including, not only Cash Flow Analysis and Profit and Loss reports but also Previous Year Comparison Reports that can help you see where you have been, the strides you have taken, and how best you can improve your game plan moving forward. With Microsoft Excel, you will need to enter the information more than once – even if it means copying and pasting field items and re-configuring codes, it is very time consuming, non-productive, and limiting. According to Fran Burns – Contributor at CFO Tech Outlook, “It’s time to stop ignoring the ‘elephant in the room’ and focus on integrated solutions that enable one version of the truth.”

“The number one disadvantage of using Microsoft Excel for accounting is the lack of its ability to reconcile accounts, which is the most important aspect of accounting.” Eugénie M. Nugent

As a liaison working on the front line bridging the gap between many CPA’s, CFO’s and their clients, I have seen firsthand the dilemma they are faced with from clients who refuse to use anything other than Excel for their accounting, yet require accurate financial analysis and advice from their CPA’s and CFO’s based on the limited construct of Excel spreadsheets they have tabulated. As I have come to realize, many of these clients choose to stick with spreadsheets because they are intimidated by these software; even when they have delegated their bookkeeping, they feel a sense of not knowing what is going on behind the scene, and this unfamiliarity has kept many of them from stepping on board the integrated financial solutions software train. I have the responsibility to steer those clients to the right software, in order for them to be able to get what they need as far as their personal or business financial analysis – which their CPA will not be able to provide them with – if there financials aren’t compiled in a way such that relevant reports can be accessed and generated, and so I have developed one-on-one customized training modules for these business owners using QuickBooks, which has resulted in a paradigm shift.

Microsoft Excel is a multidimensional, multifaceted macro programming language software that has earned its place in the business world and the world in general; however, it is not an accounting software – was not designed with accounting in mind, and therefore should not be used as your main accounting tool. If you are a business owner who is serious about having the right information to help you make good business decisions, you must use an integrated financial solutions software for your accounting. If you must use Excel in your business reporting, use it to configure and house data that you have compiled using an integrated financial solution software.

by Eugénie M. Nugent | May 31, 2016 | Business Improvement, Business Tips

Photo courtesy of APO Bookkeeping

The fact that you are reading this means you have thought about it. But would you have been interested in a “cloud based” accounting and bookkeeping application a few years ago? Probably not! Like myself and many small business owners, you were probably still trying to get your arms around the cloud and doubting that you would ever entrust your most critical financial data to some outside company. But times have changed. Online, or cloud financial applications are slowly but surely becoming the norm, and many small business owners are taking notice, particularly because of their benefits.

There are many cloud accounting and bookkeeping applications available on the market to date for small businesses. Some of them are: QuickBooks Online, Cheqbook, Xero, FreshBooks, Kashoo, Zoho Books and Wave. Most of these programs are pretty simple to use, and with only the bare basics of accounting, anyone should be able to use them. These programs also make it easier to have someone else do your bookkeeping while you maintain your Invoicing and receivables simultaneously from anywhere there is an internet connection. They can be accessed on a smartphone, tablet, or computer. This means that you have options! You can outsource your entire bookkeeping and accounting processes, or elect to have specific portions outsourced.

Benefits of Cloud Accounting

1. Cloud Based Accounting is Safe and Secure

When it comes to your company’s finances, nothing is more important than keeping your sensitive information from leaking out, which could have disastrous effects on you and your business. With a cloud based virtual accounting solution, your data is stored on a secure server. When you need to send data back and forth, it is done using only the highest available level of encryption, which keeps the data from being read – even in the unlikely event that someone could intercept the transmission.

2. Cloud Accounting is “Always On”

O the convenience of easy access! One of the reasons that cloud based accounting is becoming so popular is that it provides a level of coverage that you could only get otherwise by hiring an entire accounting department. Most small businesses cannot afford the expense of hiring even one full time staff member, and will generally bring someone in to do the books on a part time basis as needed. That may only be once per month to a few days a month, which leaves a lot of gaps if there are critical needs on the off days. With these applications you have the option of using a virtual bookkeeper and even accountant, which will undoubtedly cost less while keeping your accounts updated. Even at nights while you sleep, your accounts can be updated. You can choose to have a team assigned to you by some of these companies for full coverage, if you prefer to have the same company personnel rather than other remote bookkeepers do your bookkeeping. Regardless of how you choose to handle your bookkeeping, using any of these cloud accounting applications will allow you and whomever you give permission, to have access to your data 24/7 from anywhere with an internet connection.

3. Cloud Based Accounting Applications are Versatile

Cloud based accounting applications have something that only the cloud can provide. Because these applications are located online, they are better able to be integrated with many other applications that are designed to work with them, offering customized solutions to various business needs. Ecommerce and payment processing solutions such as Shopify, Paypal, Square etc. work seamlessly with these programs. QuickBooks Online has the widest market of these software applications, and as such, there are many more applications available that can be easily assimilated with it.

4. Cloud Based Accounting Allows for Seamless Collaboration

Since these applications are cloud based and hosted, they allow for easy and seamless collaboration. You and your business partner, for example, may be in different locations but need to look at and discuss your numbers. These online programs make this possible!

Downside to Cloud Accounting

1. These applications often become overloaded and thus slow running, depending on the time of day. During regular business hours of 9 through 5 when most businesses are open and staff working in QuickBooks, there may be times when it becomes really slow.

2. Cloud based accounting applications are sometimes inaccessible. There may be times when you have work to do but the application is inaccessible or unavailable for any number of reasons.

3. You Cannot Backup Your “In the Cloud” Data. Because these applications are not on your system, you cannot backup your data, and will need to wholeheartedly trust these companies to have your data available whenever you need to access it.

Technology has advanced in a myriad of ways, and people who are not excited about the new way of doing things are forced to either move with the time, or be left behind. Many accounting software companies who started out with desktop accounting software are moving rapidly towards closing them out altogether. Although you may have purchased the desktop edition and it is yours to keep, you may not be able to use it the same way you usually do. For example, if you use your QuickBooks desktop software to generate payroll and depend on the updates from Intuit to get them done accurately, you will not be getting those updates anymore. If you are only using it for financial record-keeping, invoicing, etc. then you should be ok with it. Otherwise, you will need to switch to the cloud. Eventually that is the only option we will have! So, it is probably a great idea to get on board and transition sooner than later.

My Personal Preference

Desktop hosted applications. Call me old-fashioned, but I like to feel that I have control over my financial data. But what good is having the desktop software when they are no longer supported by their makers who strip away the minimal functionalities they have, such as the ability to email your Invoices through the software for quick payments, and generate your employees payroll?

by Eugénie M. Nugent | Oct 29, 2015 | Business Improvement, Business Tips

Photo courtesy of APO Bookkeeping

For any number of reasons, you may opt to do your bookkeeping on your own instead of hiring a bookkeeper in-house or outsourcing your bookkeeping. Like many things, there are advantages and disadvantages to doing your own bookkeeping, but with some basic accounting knowledge and a keen eye for detail you should be able to pull it off. Here are a few tips to help you as you do it on your own:

Use the Right Accounting System

Use the Right Accounting System

Accounting is either cash-based, or accrual-based. With the cash method, you count the income when you receive it, and expenses when you pay them. Under the accrual method, you count income and expenses when they happen, and not when you actually receive or pay them – respectively. The other main difference between the two methods is the ability to budget accurately. Accrual method of accounting allows for better budgeting and planning because it looks at when liabilities are incurred and revenue earned and not when cash is paid. This method puts on the books liabilities that might otherwise be forgotten, like accrued interest. The cash method does not take accrued interest into account until it is required to be paid. This could put a strain on a small business that did not plan to pay out accrued interest balance, and is now faced with cutting expenses in other areas to have enough cash to pay the outstanding balance. The two methods have their advantages as well as disadvantages, and as far as filing taxes, the IRS only requirement is that you use the accrual-based system if your annual sales is more than $5 million or you store inventory.

Record transactions as soon as they occur

If you are using spreadsheets for your bookkeeping, or doing it manually on paper, you need to record your transactions as soon as they occur. If you are using an accounting software such as QuickBooks, you need to decide whether you will be recording transactions as they happen or adding them via the bank downloads later. Regardless of the method you use, keep your books updated at all times. Doing so will allow for little to no discrepancies, better workflow, and you will also have updated information on which to rely for decision making.

Record all business transactions

In order to have accurate numbers from which to make good business decisions, and file correct tax returns, you need to ensure all numbers affecting the business is accounted for and recorded. For example, if you are a business owner who sometimes uses personal funds for business expenses – and vice versa, you need to include those numbers in your bottom line.

Track Reimbursable Expenses

As a Small Business owner, it is very likely to sometimes use your personal funds to for pay business expenses. These monies should be reimbursed to you as well as recorded in the company’s expenses, and so there should be an account created to keep track of these reimbursables. Also, if your employees are construction workers or engineers who are usually in the fields and may use their funds to make small purchases that are immediately needed in order to continue their work, you need to collect those receipts and add them to the reimbursable account from which you will later repay them. Doing this is also important for accurate job costing.

Keep Accounts Categorization Simple

Overcategorization leads to miscategorization and ultimately inaccurate reporting. As a small business, you should be able to categorize your accounts in three to four sections:

1) Income – under which you can create subaccounts of your various streams of income

2) Cost of Goods Sold or Cost of Sales – under which you can create sub accounts for the employees salaries who are directly involved in the creation of the products you sell or the services you offer, as well as the products purchased to be used in the creation of your complete product for sale.

3) Operating Expenses – under which you can create a subaccount for Administrative Expenses and further subaccounts under Administrative expenses to list those individual accounts.

4) Other Expenses – under which you can create subaccounts to list other expenses that do not fall under any of the above categories.

The balance sheet accounts are usually fairly standard with three main sections: 1) Assets, 2) Liabilities, and 3) Equity each with their own subaccounts. You will need to create additional accounts on as needed basis. For example, if you loan money to your company, you will need to create a liability account to record these amounts the company owes you. Likewise if you borrow money from your company, you will need to create an asset account to reflect this.

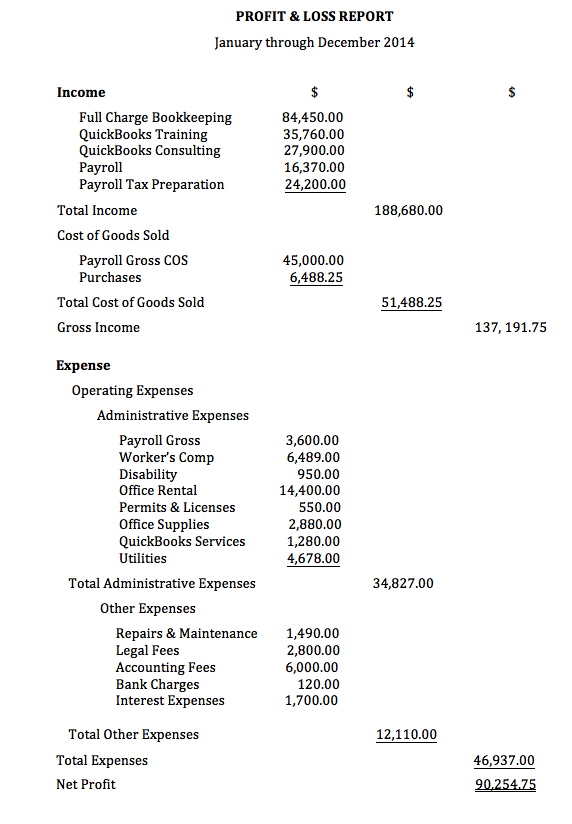

Here is an example of a Simple Profit & Loss Report or Income Statement:

Deduct Sales Tax from Total Sales

If you are a retail business that collect sales tax on behalf of the government, you should deduct these sales taxes from your sales. If you are using a software such as QuickBooks for your bookkeeping, and you do not track inventory in QuickBooks, you can setup this account as an Income account and set it as a discount so that it will be listed at the top of your Profit and Loss report and lessen from the total sales. Also, avoid penalties and interests and pay over your sales taxes as soon as they are due.

Keep Proper Records of Loans Received

Many small business owners need financial backing at their startup, and may take out a loan or two. These loans must be recorded and tracked in separate accounts, paying special attention to separating the principal repayment and the interest payment. The interest is an expense to your company and should be recorded in the expense section of your income statement or profit and loss report, while the principal is made towards your loan balance which will be in your liability section of your balance sheet.

Use Checks or Credit/Debit Cards Instead of Cash

Cash makes it harder to keep track of spending. Misplaced receipts, forgetting to document purchases all can be avoided if checks or debit/credit card payments are made. Not only will you have the amounts available to record, but you will also have details on uses of funds.

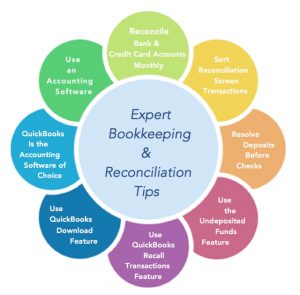

Reconcile all Business Bank & Credit Card accounts every month

This is one of the best business practices to employ! Reconciliation is a fundamental aspect of bookkeeping. Not only will you be able to catch any mishaps that occur; it will spread your workload and keep your books up-to-date-and accurate. Also, any mistakes on the bank’s or credit card company’s part that are not caught within six months, will not be able to be resolved. If you look on your statements, you will see that the banks include a reconciliation sheet and recommends that you reconcile your numbers with theirs. Reconciliation is the only way to ensure your numbers are accurate and your bookkeeping on par.

Let Payroll Specialists Handle Your Payroll

Payroll and payroll taxes can be complicated/intricate and not only do you need to ensure your employees paychecks are precise, but you must make correct payroll deposits as well as file accurate taxes. Payroll specialists are trained especially for this, and so they know the ins and outs, and are fully equipped to get this done accurately.

Keep a Proper Filing System in place

Not only is this good business practice, but you do not want to drive yourself crazy trying to find one document that is urgently needed – pronto. As a “do-it-yourselfer” it will greatly benefit you to keep a proper filing system where you will file all documents and paperwork in a manner that makes them easily retrievable.

Keep an Eye on Your Cash Flow

Cash is King for any business, and the lack of it is the reason so many small businesses fail. Know how much it takes to keep your business running on a monthly basis! Devise an accurate system of expenses and monthly obligations, and weigh them against your reliable monthly inflow of cash. Include an extra 20% of total expenses to your expenses for a bit of “cushion”. A budget and forecast report is a huge plus to create, maintain, and use as a financial guide.

Give Your Customers Options to Pay You

Providing your customers with a variety of payment options will not only make your customers happy as far as convenience, but it will allow you to get paid more quickly. In today’s fast paced world, convenience goes a long way! Some customers may procrastinate writing that check AND mailing it, or setting up that online bill pay. Allowing them the option to pay you via your submitted invoices will be a huge plus in helping your cash flow.

Invoice Customers on Time

The sooner you bill your customers the sooner you will get paid, and that will also help keep your cash flow up and your budget on track.

Pay Bills on Time

Pay attention to those vendors who are sacking a late payment fee to late payers. Take advantage of those terms of payments you get, but make every effort to meet them. The delay will help with your cash flow, but may accrue interest if not paid on time.

Have your vendors submit a completed and signed W9 form

For vendors to whom you have paid a minimum of $600 and above during the year who are not a corporation, you will need to report their payments to the IRS on from 1099-Misc at the end of the year. You will need specific information from them to include on this form such as their mailing address and tax identification number. It is best to keep W9 forms on hand, so that you can have your vendors complete them at the time you realize that the monies you are paying them are at this threshold. You should check your vendor balances to see if the monies you have paid them are amounting to $600 and above, as you may often write a check for under six hundred but may make more payments to them amounting to $600 and above throughout the entire year. Waiting for year-end to collect this information may be a daunting task, which many times – from my experience, has proven futile. You cannot file form 1099 without the vendors tax identification numbers, and of course you will need to mail their copies to them. If you pay your vendors through a Payment Portal such as Paypal or with your credit card, you will not be required to file or include those amounts on your 1099 as these companies are already reporting them on their 1099k.

Backup Your Computerized Information

Computerized systems as well as software do fail at times, and it would be devastating if all the work you have put in to your system were to become corrupt beyond repair, or inaccessible. Portable Hard Drives like this Toshiba Canvio Connect II 1TB Portable Hard Drive or this Seagate Backup Plus Slim 2TB Portable External Hard Drive with Mobile Device Backup USB 3.0

or this Seagate Backup Plus Slim 2TB Portable External Hard Drive with Mobile Device Backup USB 3.0  will store a copy of your information for easy retrieval, and save you the headache of ever losing your information that you have worked so hard at compiling.

will store a copy of your information for easy retrieval, and save you the headache of ever losing your information that you have worked so hard at compiling.

Leave an Audit Trail

If you have a system that allows you to quickly and easily retrace your company’s financial activities, your record keeping is effective. This includes keeping your invoices and checks in numeric order, not skipping check or invoice numbers, and keeping bank and credit card accounts separate. You should be able to retrace a year or years and have a clear trail of your company’s financial activities.

The best way to work as a “do it yourselfer” and not be overwhelmed, is to always keep every area of the business up-to-date. Designate a time to get the tasks that can be done later such as recording reimbursables and paying bills, and do the ones that cannot wait – such as Invoicing and attending to your customers first. Create a monthly chart with a daily workflow that you will be able to model everyday, and stick with it.