Retained Earnings, also known as “Accumulated Earnings” and “Unappropriated Profits” is one of the most important items on the balance sheet of a business financial statement. It represents the percentage of net income that is not paid out as dividends, but instead is kept “in-house” by the company.

Any item that impacts net income or net loss will impact retained earnings. Examples of items that would impact retained earnings include: sales revenue, cost of goods sold, depreciation, and general operating expenses.

How To Calculate Retained Earnings

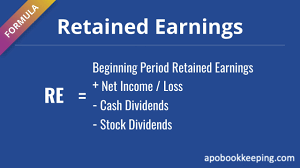

Retained earnings is calculated by adding the net income from the current period to the retained earnings from the previous period and then subtracting any net dividends that were paid to shareholders.

It is calculated at the end of each accounting period and is based on the previous period’s figure. The resulting number can be positive or negative, depending on the company’s net income or net loss over time. A company with negative retained earnings has failed to earn a profit for a predetermined period, and is therefore retaining its losses. Failing to make a profit is not an uncommon occurrence for a business since failures will happen from time to time. However, if a company fails to earn a profit over several successive periods, the business owner should carefully evaluate the business, their earning potential, and the ambitions of the company.

What Retained Earnings Reveal About Your Business

Retained earnings can reveal much about a company. They are an important indicator of a company’s financial health and business performance. For example, a high and positive retained earnings might be a sign that the company has a strong business plan; however, a company with a history of low retained earnings may be able to access more financing.

How Retained Earnings Can Benefit Your Business

Knowing the amount of retained earnings can help a business owner understand the financial goals of the company. If a company has a high retained earnings, the owner can decide to take a larger percentage of investment income to support the company and reduce retained earnings balances.

Rather than distributing the profits to the owners, the retained earnings can be used to reinvest in the business or to pay off any debts the company may have.

The retained earnings account is important because it shows how much profit a company has made over time and how much of that profit has been reinvested back into the company.

For the best bookkeeping services in New York, APO Bookkeeping has you covered. We streamline your bookkeeping processes, ensuring that everything is kept updated, manageable, and above all – effective. Let’s have a chat—reach out to us today to learn more.

Doing your own small business bookkeeping can be a very simple process; however, there are things that must be in place to ensure you are doing it correctly so you can retrieve accurate reporting from which to make good business decisions as well as file accurate taxes.And no, there is no way to avoid bookkeeping if you are running a legitimate business. You can hire a New York City bookkeeper to do your bookkeeping in-house or outsource your bookkeeping to a bookkeeping and accounting Firm – like ours, but your business bookkeeping must get done. Why? Because bookkeeping is an important part of running a business. It allows you to track the financial health of your business as well as keep your business in compliance with the relevant tax authorities by filing accurate and timely taxes.

What is Bookkeeping?

While accounting is the process of interpreting and communicating financial information, bookkeeping is the systematic process of identifying, classifying, recording, organizing, verifying, and managing daily financial transactions of a business.

How to Get Started With Your Own Bookkeeping

Having a defined framework is essential to starting and maintaining an effective bookkeeping system. In this article, we will be outlining 5 important steps that will help you as a small business owner, set up and maintain a proper bookkeeping system.

1. Choose an Appropriate Accounting Software

Accounting and bookkeeping software makes it easier to do bookkeeping. Some accounting software such as Sage 50 require extensive accounting and bookkeeping knowledge in order to use it correctly, while others such as QuickBooks allows you to use it with basic accounting and bookkeeping knowledge. It is very flexible, multi-functional – integrating with multiple apps, and allows for the production of a myriad of reports. Whatever you do, do not use an excel spreadsheet to do your bookkeeping, because not only is it inflexible, but it does not allow for the reconciliation of the accounts, and as such it has a large margin for error. Reconciliation is central to the bookkeeping and accounting process and a good bookkeeping and accounting software provides for the reconciliation of bank, credit card, loan accounts etc.

2. Set Up a Chart of Accounts

The Chart of Accounts is the backbone of the accounting and bookkeeping system. It is where information is stored to be retrieved via reports and thus need to be associated with the right account type in order to appear on the right reports and in the right places – making the reports correct. The Chart of Accounts should be specific to your business and workflow, however, every transaction must fall in one of five categories of accounts: 1) income, 2) expense, 3) asset, 4) liability, or 5) equity.

Income account:This account records all the revenue the business generates for example revenue from the sale of inventory.

Expense account: This account records the cash outflows from the business for example payments of salaries to employees.

Asset account: This account records all the resources owned by the business for example property and inventory.

Liability account: This account records all the debts and financial obligations the business owes for example a business line of credit.

Equity account: This account provides a financial representation of the ownership balance of the business for example all business assets minus all business liabilities.

A good bookkeeping software will have a general Chart of Accounts to get you started and you can easily customize it to suit your unique business needs.

3. Separate Your Business & Personal Finances

Keeping your business and personal bank and credit card information separate will not only save you the headache of being extremely careful with each transaction every time you are entering them, but it will ensure you are getting accurate business reports from which you can make informed business decisions as well as using accurate information to file your taxes. Keeping your business financials separate from your personal finances will also help protect your assets in the case of any legal actions against your business. Accounting and bookkeeping software such as QuickBooks allows you to setup more than one business or company, so you can setup your business and your personal in two separate QuickBooks areas.

4. Reconcile Your Accounts & Balance Your Books

Without reconciliation your bookkeeping is incomplete and the accuracy of your books is unknown. Your transactions in your software should be tallied and compared with the transactions on your bank statements for example, and they should all match up. In addition, when you compute each months’ debits and credits, they should match up. This will mean that your books are balanced and the bookkeeping process is complete. You may choose to balance your books at the end of every day, week, month, quarter, or year.

Once you combine the different account types, it should meet the accounting equation: Assets = Liabilities + Equity, but don’t worry, as long as you enter the transactions in their right accounts and corresponding category types, software such as QuickBooks computes it all for you.

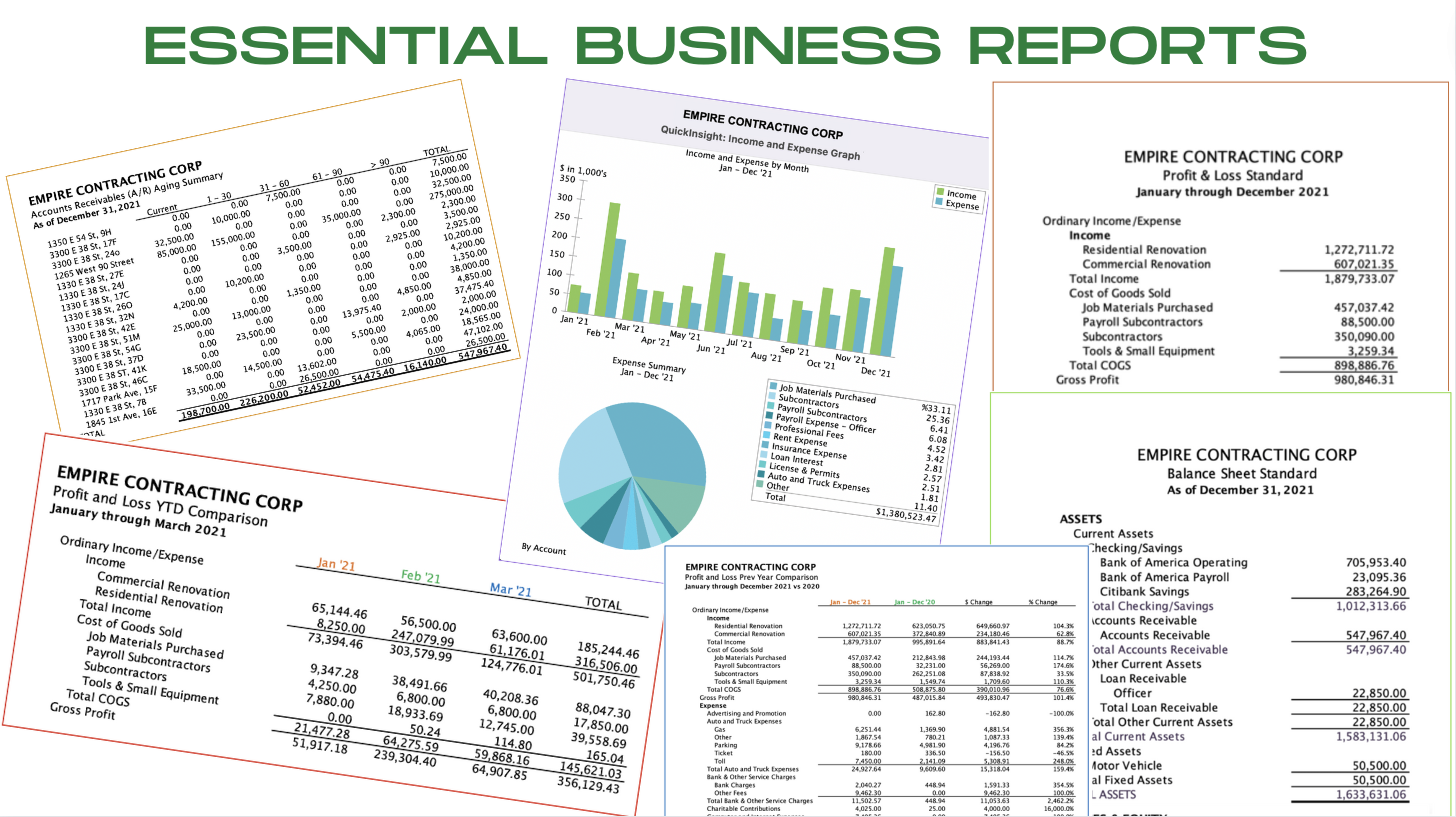

5. Generate Financial Reports Periodically & Analyze Them To See Where You Are Financially

It is very important to generate financial reports at regular intervals so you can get a clear picture of the financial health of your business. The three crucial financial reports are the balance sheet, profit and loss (P&L) or Income statement, and the cash flow statement.

The balance sheet summarizes the total assets, liabilities, and equity of the business. It indicates whether the business can expand or needs to reserve cash. The (P&L) statement or the income statement breaks down the revenues, expenses, and costs of a business over a period. It can enable you to compare sales and expenses and make accurate forecasts. The cash flow statement enables businesses to know their ability to fulfill short-term financial obligations.

Every business must get bookkeeping done regardless of how small they are, and the good news is there are qualified bookkeeping professionals available to handle the bookkeeping, if the business owner would prefer not to, or does not feel qualified enough to handle it.

At APO Bookkeeping, our bookkeeping services for small businesses protect business owners from making costly mistakes and provides valuable insights on how they can grow. You don’t have to be a math genius to start implementing bookkeeping for your business but you must be consistent and the foundation must be accurately laid. With this simple framework, you can start implementing bookkeeping today!

There is so much you can get from Excel spreadsheets, and no more! Don’t get me wrong, Microsoft’s Excel has its many purposes one of which is capturing information and making calculations including statistics with useful bars and graphs resulting in eye-catching, aesthetic presentations; however, it does not have the capacity to convert information from one report type to another, reconcile entries, or provide real-time bookkeeping and accounting stats, and therefore cannot provide the cross-reporting intelligence analysis that businesses need in order to facilitate strategic planning and make good business decisions. It is not enough to know how much profit has been made thus far for the current year, or how much your current expenses are; businesses must be able to look comprehensively at their business stance at any given moment, if being successful and staying in business for the long haul is their main goal.

Use an Integrated Financial Solution Software for All Your Business Accounting Needs

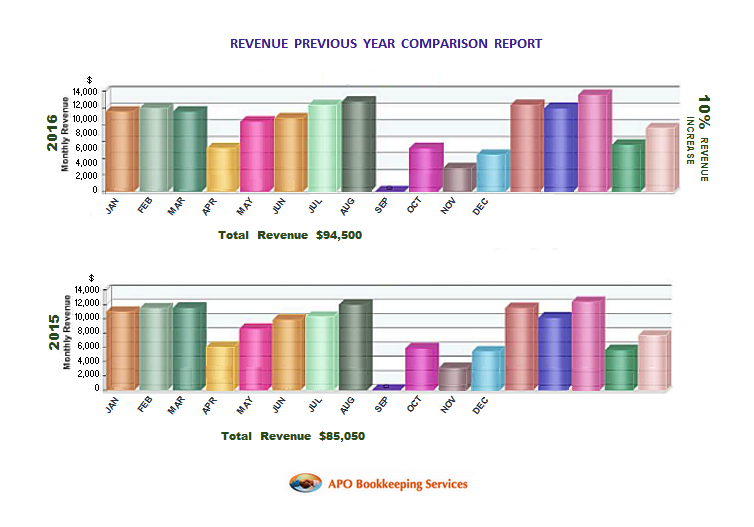

This is where cross-reporting, intuitive, integrated financial solutions software such as Intuit’s Software – QuickBooks, and Sage Peachtree come in. With an integrated financial solutions software, you enter the information once, and you get to use that same information in a variety of ways to pull insightful reports including, not only Cash Flow Analysis and Profit and Loss reports but also Previous Year Comparison Reports that can help you see where you have been, the strides you have taken, and how best you can improve your game plan moving forward. With Microsoft Excel, you will need to enter the information more than once – even if it means copying and pasting field items and re-configuring codes, it is very time consuming, non-productive, and limiting. According to Fran Burns – Contributor at CFO Tech Outlook, “It’s time to stop ignoring the ‘elephant in the room’ and focus on integrated solutions that enable one version of the truth.”

“The number one disadvantage of using Microsoft Excel for accounting is the lack of its ability to reconcile accounts, which is the most important aspect of accounting.” Eugénie M. Nugent

As a liaison working on the front line bridging the gap between many CPA’s, CFO’s and their clients, I have seen firsthand the dilemma they are faced with from clients who refuse to use anything other than Excel for their accounting, yet require accurate financial analysis and advice from their CPA’s and CFO’s based on the limited construct of Excel spreadsheets they have tabulated. As I have come to realize, many of these clients choose to stick with spreadsheets because they are intimidated by these software; even when they have delegated their bookkeeping, they feel a sense of not knowing what is going on behind the scene, and this unfamiliarity has kept many of them from stepping on board the integrated financial solutions software train. I have the responsibility to steer those clients to the right software, in order for them to be able to get what they need as far as their personal or business financial analysis – which their CPA will not be able to provide them with – if there financials aren’t compiled in a way such that relevant reports can be accessed and generated, and so I have developed one-on-one customized training modules for these business owners using QuickBooks, which has resulted in a paradigm shift.

Microsoft Excel is a multidimensional, multifaceted macro programming language software that has earned its place in the business world and the world in general; however, it is not an accounting software – was not designed with accounting in mind, and therefore should not be used as your main accounting tool. If you are a business owner who is serious about having the right information to help you make good business decisions, you must use an integrated financial solutions software for your accounting. If you must use Excel in your business reporting, use it to configure and house data that you have compiled using an integrated financial solution software.

Are you a small business owner trying to manage all aspects of your business on your own?

Have you fallen behind with your bookkeeping?

Do you find that your bookkeeping tasks are taking the passion out of your business?

Do you pull your hair out every time you think about keeping the books? (Well, not literally, I hope)

Let us help you! We specialize in catching up the books and then continuing to keep them updated. We have helped countless small business owners – sole proprietors, partnerships, LLCs, and S-corps – with their bookkeeping needs. Whether you’ve fallen behind (by a month or two or even by a whole year or two) or just don’t want to deal with the process of working on the books each month, we can help!

Being behind on your bookkeeping unfortunately means being behind on your business stance. If you are not monitoring your numbers in a visible form and generating insightful reports, you could definitely find yourself out of cash flow and ultimately out of business.

We provide services on and off-site to clients in the New York metropolitan region, and remotely in all other geographical areas of the continental US. We assist small to mid-sized businesses across industries.

Most small business owners are surprised to discover that our bookkeeping service packages are extremely cost-effective and our services actually lead to increased profits, reduced taxes, and improved cash flow – not to mention fewer headaches and more time for doing things you love and more hours you can use to focus on growing your business.

Reconciling all your accounts on a monthly basis is the single most important thing you could do for yourself and your business. There are numerous software available to help make this process effortless, but regardless of the software or lack thereof, monthly reconciliations must be done in order to avoid costly mistakes.

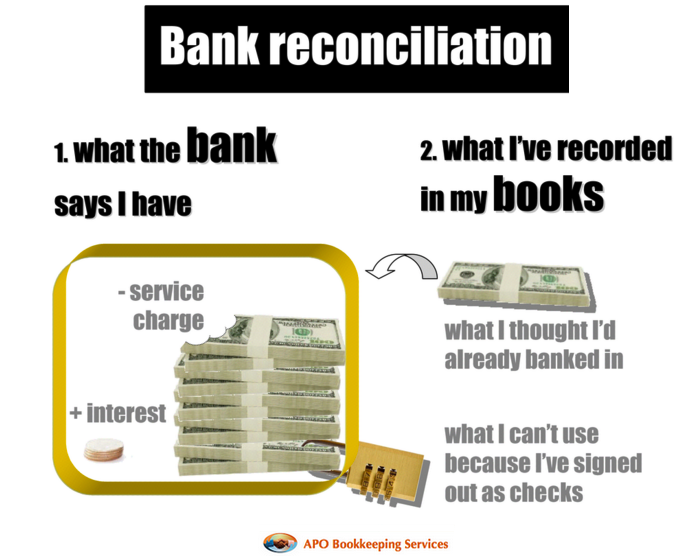

Why reconciling your accounts is so important

Reconciliation is so important because it is the only way to be certain your account balances are in agreement with your financial institutions, vendors, etc. Reconciling your accounts ensures that the actual monies spent matches the monies leaving an account at the end of a period, and that the actual monies put in also matches the monies coming into an account at the end of a period. When you reconcile your bank statement every month with your QuickBooks balance for example, you will become aware of checks that have not been cleared, and this will help you track down any potential missing payments. You will also become aware of any deposits you have made that are not showing up. This is rare, but it does happen! In addition, you can use your reconciliation statement to make sure your other company transactions are going through and have been calculated for the proper amounts.

There are aspects of your financials that reconciliation will not take care of such as personal monies you used up for the business, but have not recorded, as well as other assets and liabilities that may not have affected your reconciliations. So, reconciliations alone will not make your “books” accurate. You may need the help of a bookkeeper and CPA to get these aspects worked out; bookkeeper to ensure everything is recorded, and the CPA to analyze what is recorded and make the final call on whether the entries make the final books better or worse for the business.

It is imperative that controls – checks and balances, are in place to monitor the business banking and credit card transactions. For large firms you should have multiple hands assigned to cross-checking banking activities on a regular basis. For small businesses, you the owner should check your banking transactions – at least on a monthly basis to ensure everything is on par – even though you may have someone assigned to reconcile your accounts. When bank statements are not monitored and reconciled, the potential for undetected loss is high. Not all employees or accounting firms are honest, and you may not miss money that has been taken for some time. This is the reason some employees are able to embezzle hundreds if not thousands of dollars over time. Reconciling your bank statement helps you prevent losses and may indicate a potential problem in your accounting system.

What accounts can be reconciled and how to reconcile them

Any account that you get a statement for, showing a beginning and ending balance, can and should be reconciled. This includes: bank accounts, credit card accounts, loans and lines of credit accounts, and vendor accounts. There is also the internal reconciliation of many accounts, including customer receivables accounts.

Reconciling any account in software such as QuickBooks is a moderately easy feat. The time it takes to reconcile your accounts will depend on the accuracy of the transactions entered in your accounting system; if they were entered correctly – precise numbers and debit/credit accounted, your reconciliation should be done in a shorter time. If however they were not carefully entered, it may take you a longer period of time trying to locate the discrepancies. If this is the case, you may need to go transaction by transaction verifying your bank statement numbers with QuickBooks and marking each cleared as you go along. This can be tedious if there are many transactions; however, it must be done. You can see why it is vital to enter all transactions accurately to begin with. If you are using QuickBooks or other similar software, you should take advantage of the “download” feature. Initially, you will need to edit and select the right accounts as well as input the vendor or customer before you add or match each transaction; however, QuickBooks will begin to recognize each transactions that you have edited after a while and most importantly your numbers will be accurate with the correct corresponding debit or credit.

Using the ask my accountant account for questionable transactions

QuickBooks has a “Ask My Accountant” option in their chart of accounts that can be a huge ally in helping you reconcile. At times you may have transactions that you are not sure how to enter, or how to enter to be beneficial to your business. Any questionable transactions should be coded to “Ask My Accountant” so that you can continue with your reconciliations while having a conspicuous account to house them and have them easily accessed and rectified at a later date by your CPA.

So, reconcile your accounts on a monthly basis! You want to ensure that all the transactions are in your ledger and accurately accounted for. It is easy to forget to enter an expense or a payment when you are in a rush or if you have misplaced a receipt, so cross-checking against the account statement can be a good safety net for your own books. Doing so will ensure that you are getting paid—and paying people back—promptly, which in turn will help you keep other parts of your accounting in order such as your cash flow, profit and loss statement, etc. Of course you can trust your suppliers and creditors to charge appropriately, but everyone makes mistakes and are prone to err.

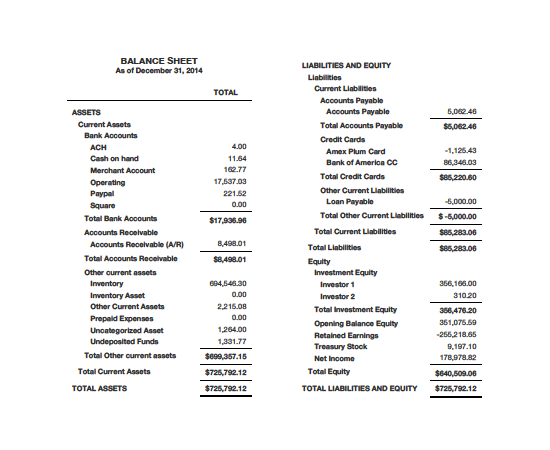

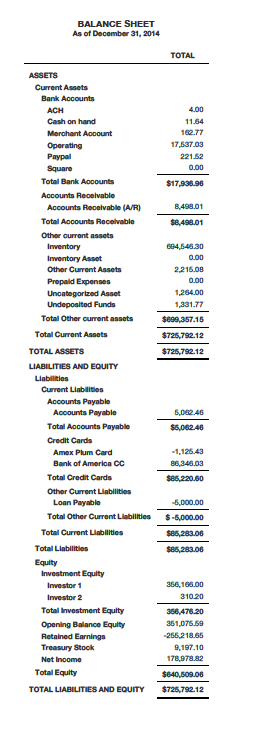

The Balance Sheet is an important report in your financial statements that shows the ending balances of what you own, what you owe, and how much you have invested in your business since its inception, as at a particular date. It is divided into three (3) main categories:

Assets

Liabilities

Equities

1) Assets – What You Own

Balance sheets usually start with cash balances that include monies presently in your bank account(s) as well as your petty cash till, minus checks you may have written but are not yet presented to your bank to be cashed. Those outstanding checks would reduce your account balance(s) once they are cashed. Monies in your Paypal, Square or any other ecommerce portals that allow you to receive payments are also shown in this section of your balance sheet.

If customers owe you money that you have invoiced for but not yet received, you will see those outstanding amounts in Accounts Receivable on your balance sheet.

If you sell products, the cost of all of them that you have purchased and not yet sold will be in the Inventory Asset account.

If you own equipment, furniture, vehicle or something similar that lasts for years, you will have a balance in Fixed Assets for what you paid for these items. If it has been a while since you have owned them, you may have a Depreciation account, and when you net the two, your Fixed Asset values are reduced.

All of the above are assets and they are listed in the first section of a balance sheet.

2) Liabilities – What You Owe

If you owe money for taxes, to vendors, or to employees, then it will show in the Liabilities section, which is the second of three major sections of a balance sheet. Day to day unpaid bills are in an account called Accounts Payable, and separate accounts are usually set up to document monies owing for taxes, etc.

If you have bank loans, they usually each have a separate account like a bank account does. Each bank loan account represents the principal due on a loan (the interest you pay is recorded in the expense section of the P & L).

3) Equities – All Monies You have Invested In Your Business Plus/Minus Its Income or Loss

The final section of the balance sheet is the Owner Equities. It is the section that will vary the most depending on the type of entity your business is set up as. For example, if your business is a corporation, there will be a common stock account that will represent the original amount of money you put into the business. It will match the Articles of Incorporation that you drew up when you incorporated. This amount will rarely ever change for the life of the business.

Also, there is usually an account called Paid-in Capital which is how much additional money you have put in or taken out of the company beyond the common stock balance.

A corporation will also have a Retained Earnings account. This reflects accumulated profit (or loss) through the years of operation.

If your business is set up as a partnership, the equity section will include an account for each partner that represents their balance in the firm, which is the net amount of money they have put into the business over the years minus the amount they have withdrawn as well as plus or minus the business income or loss through the years.

Unlike the Profit and Loss or Income Statement accounts that are zeroed out at the end of each accounting period, the balance sheet accounts accumulate continuously and does not clear out at the end of each accounting period or year. Thus, the P & L or Income Statement report can be generated using specified date range while the Balance Sheet report can only be generated as at a particular ending date and not by range of dates.

Doing your own small business bookkeeping can be a very simple process; however, there are things that must be in place to ensure you are doing it correctly so you can retrieve accurate reporting from which to make good business decisions as well as file accurate taxes.And no, there is no way to avoid bookkeeping if you are running a legitimate business. You can

Doing your own small business bookkeeping can be a very simple process; however, there are things that must be in place to ensure you are doing it correctly so you can retrieve accurate reporting from which to make good business decisions as well as file accurate taxes.And no, there is no way to avoid bookkeeping if you are running a legitimate business. You can